Think about a great skill you have. It doesn’t have to be something big or something that took years to develop, just a skill that you know makes you better for it. A skill that you’re proud of and ready to tell friends and colleagues about. Running is what comes to my mind for me right now (I absolutely love it, and I know it’s good for me).

Running also really works well with the point I’m about to make, which is that one of the consistently best ways to see your efforts pay off is by making the behavior a habit. During my sophomore year of high school, I decided that it was going to be the “year of running,” so I joined the track team, and I ran every single day. Eventually, I picked up my stride, until I got it exactly right.

The same goes for saving and investing. If you make investing a habit, it will be one decision you’re going to be so proud of yourself for doing. Investing regularly is how you can become an experienced investor (and improve your chances of reaching your goals).

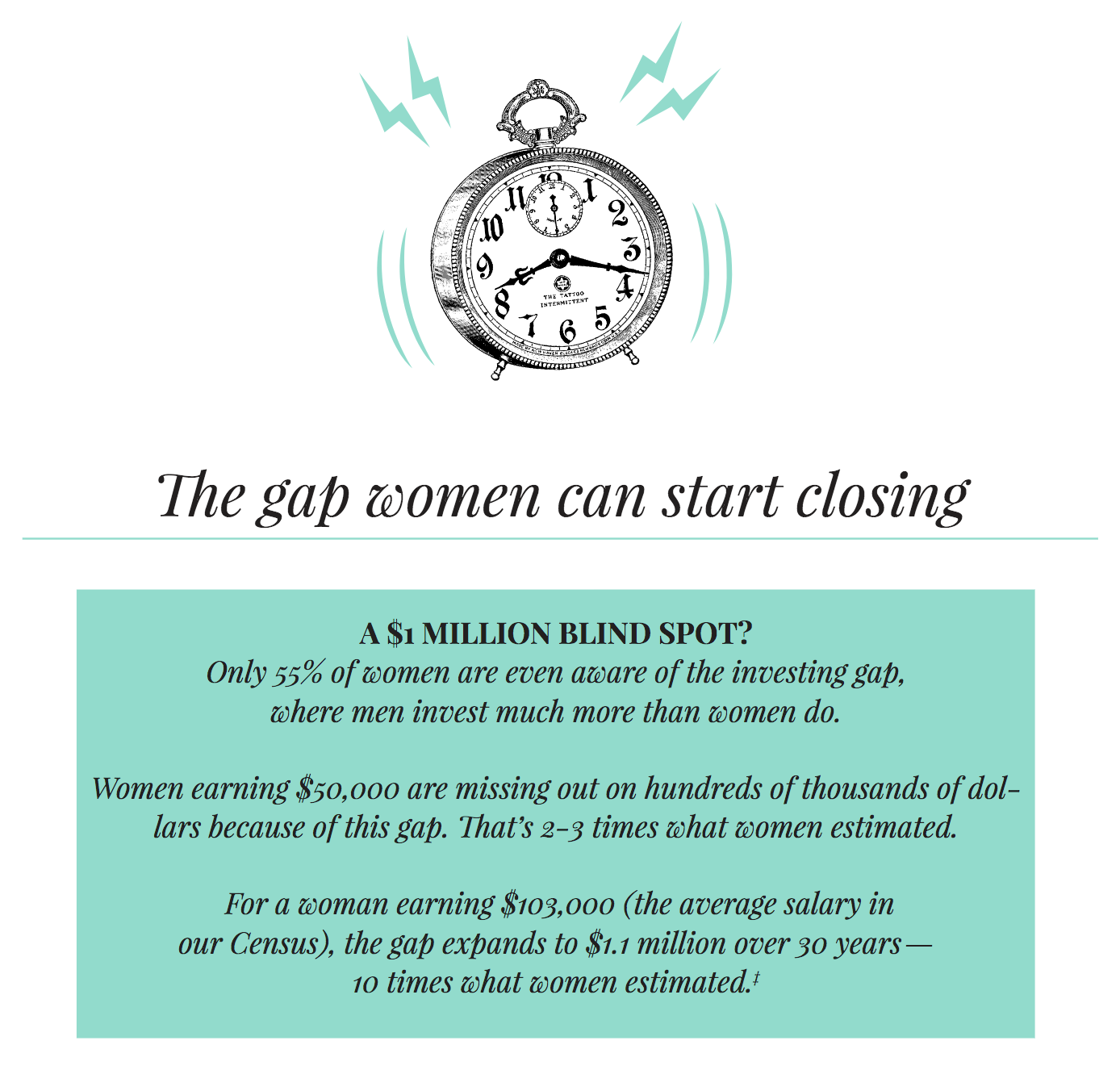

Investing is a huge wealth generator, and women, for one reason or another, tend to do it less. The result is an investment gap. Fewer women take part in the financial market, and this hurts women’s total wealth over time, thereby exacerbating the gender wealth gap. It’s a horrible, sexist financial cycle. If women earn less and don’t invest those earnings, the gap gets bigger and bigger. But, it doesn’t have to be this way. The most important thing you can do to change the investment gap is simple: Educate yourself.

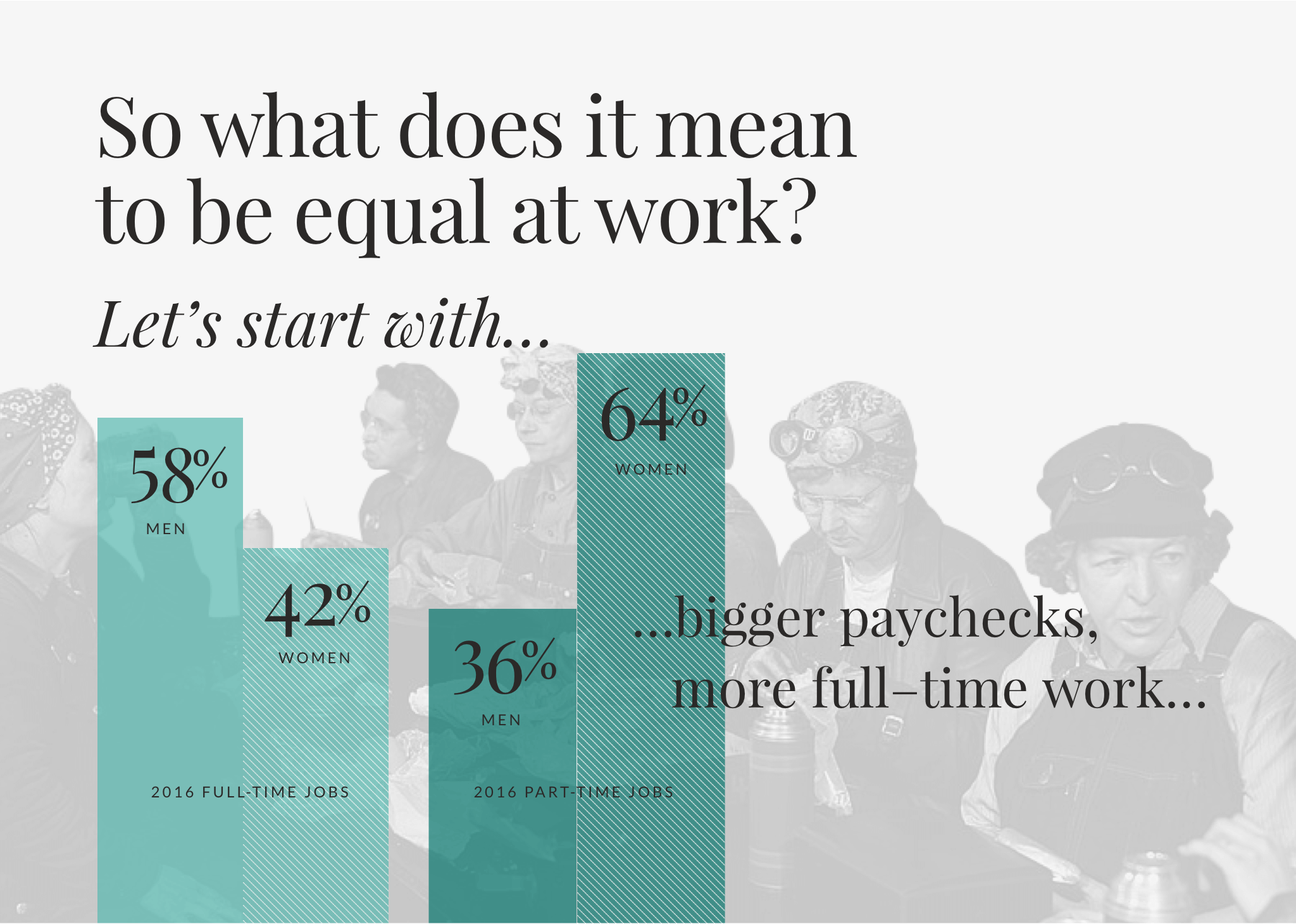

Seventy-one percent of the money women have is in cash, and any financial advisor will tell you, cash not only doesn’t earn a return; it actually depreciates over time thanks to inflation. The stock market, on the other hand, has returned an average of 9.5 percent for the past ninety years, even including the horrific downturn in 2007.

Acknowledging that a massive investing and wealth gender gap exists is one thing. Deciding how to build wealth and take action is another. If you’re a 20- or 30-something-year-old woman who has never invested, you might be asking yourself: Now what?

Taking a step back, there are three things every women—or anyone, really—can do to start growing their money.

Ready? Let’s get started.

How To Build Wealth Step 1: Start Investing (Even A Little Helps)

Number 1: Make investing a habit. A great way to get your feet wet is to start by investing a small amount. Once you get acclimated and you understand how the markets move, you can put more in.

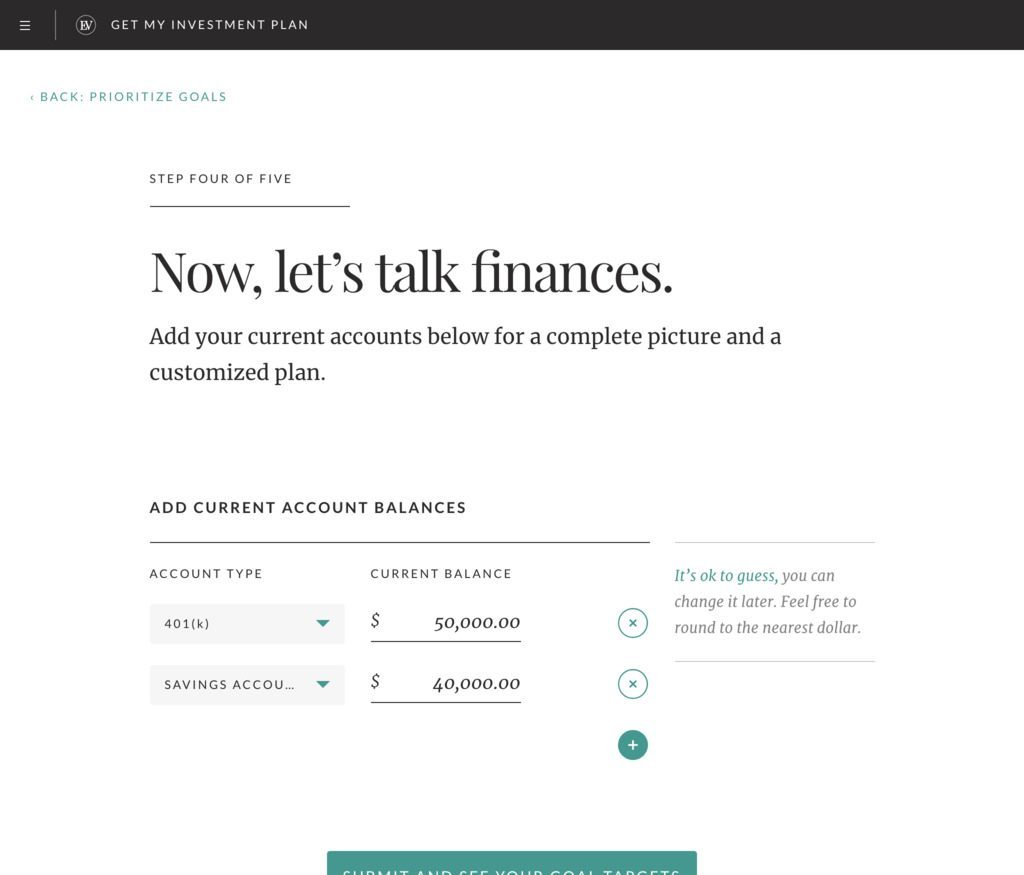

The idea that you have to have a certain amount of money saved up before you invest is fundamentally wrong. So staying of the mindset, “I don’t have any money to save or invest,’ is a mistake and it will cost you. For first time investors, working with a robo-advisor is great. Robo-advisors use technology to build really smart portfolios for people who don’t have the time, interest, or expertise to do the research.

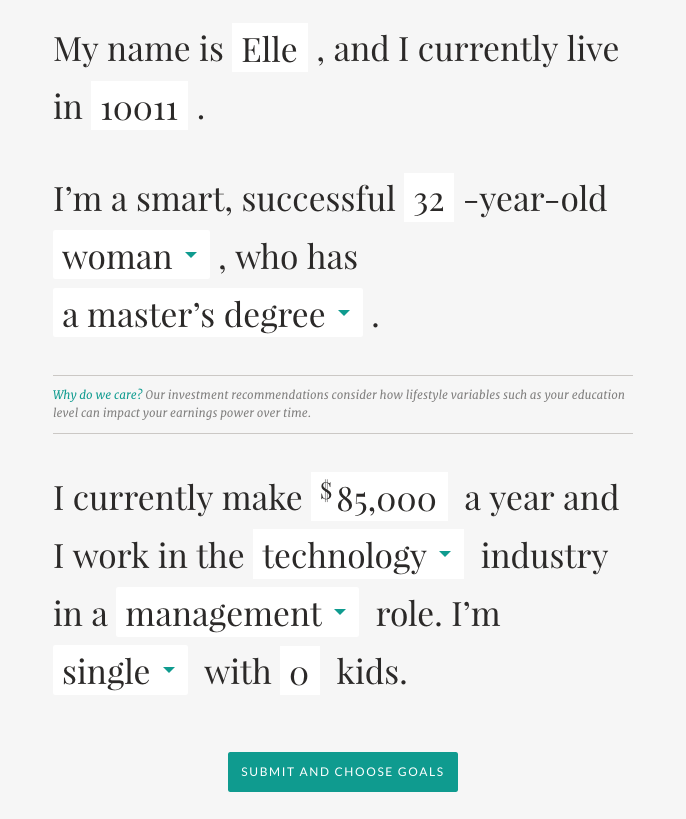

Ellevest, an unabashedly pro-female robo-advisor, will give you a free (yes, free) customized personalized investment plan to help take control of your finances right now. The way Ellevest works is incredibly simple: You sign up, answer a few of questions about how old you are, your financial situation, what you’re saving for, and then Ellevest, will instantly build you a portfolio and you can be investing in under 10 minutes with $o minimum.

How To Build Wealth Step 2: Respect Compound Interest

Number two: Starting early is important. So, don’t wait to invest. (Seriously.)

One of the most powerful weapons you can have when it comes to investing is time. This is because of the power of compounding. If you invest money today and you make money on it, the next amount of money you make is that plus the money you [already] made…and the next amount of money is that plus the money you made plus the money you made. It goes on and on.

Albert Einstein is reported to have said compounding is the eighth wonder of the world. Therefore, a dollar invested in your 20s is worth so much more than a dollar invested in your 60s.

Sure, saving money in the bank feels like a safe bet. That’s because you don’t ever see your account balance go down (unless you withdraw it yourself). But there is a risk: If you’re only saving, you may be unable to reach your financial goals. Many of us need to grow the money we save in order to reach our goals—which is what investing is all about.

Think about this: If you put $25,000 in a savings account, after 35 years of earning interest, you’ll end up with $35,391 or more, assuming a range of many different economic scenarios. And you’re guaranteed not to lose that money.

However, if you invest that $25,000 in a well-diversified portfolio consisting of 60% stocks and 40% bonds, your account will grow to $54,348 or more in 35 years, under the same economic scenarios.*

How To Build Wealth Step 3: Check Your 401(k)

Number three: Check your 401(k) to see what percentage of your income is being contributed. The default is typically 3%. So, ask yourself if that will be enough to take you to retirement and if you’re able to contribute a higher percentage. The maximum dollar limit in 2018 is $18,500.

Don’t think you have enough money to invest 2o percent? That’s OK. Start with 1 percent, then work your way to 5 percent and then 10 percent. The goal is to eventually be setting aside 20 percent of every paycheck to Future You.

Regardless of how you start to build wealth and invest, there’s plenty of motivation to begin. When Ellevest researchers asked women what drove their confidence to reach their goals, the answer was surprising.

“It wasn’t her relationship with her partner. It wasn’t how she’s doing at work. It wasn’t her level of education,” said Krawcheck. “It was how much, and if, she was saving and investing.”

So, three things. Now you know.

Pay yourself first: Your new golden rule for 2019. Make sure a cut of every paycheck goes straight to your retirement or savings account and does not pass go. Get started today.

Here are more financial topics for you…

If You Save $15 a Day, Here’s How Much Money You’ll Have in Retirement

3 Reasons You Should Have an IRA, Even If You Have a 401K

Finally: A Breakdown of How You Should Be Spending Your Money

Questions? We’re here to help. Leave us a comment and we’ll get back to you!

Wondering how much to put toward retirement and how much to invest? Every journey starts with a destination. Here’s a good perspective of how much to spend on needs, how much to spend on clothes and how much to invest.

If you don’t want to read it, I’ll give you the snapshot. You should dedicate 50 percent of your check to your personal needs, 30 percent to fun, and 20 percent to saving and investing. Follow this rule of thumb and you’ll be set for financial success over the course of your life.