It’s that time of year again: Festival season is finally here and festival style is top of mind. If you’re looking for fresh, fun and exciting pieces to wear, we’ve got you covered. For the best festival dresses, we looked to Amazon because the retailer carries a plethora of incredibly stylish pieces we absolutely love. You don’t have to spend a fortune either — all these dresses are under $40.

Curious what classifies a product as timeless? It’s a fashion piece that can withstand the test of time and look great, no matter the decade. We all know trends come and go, but a timeless piece…. that is one you can wear year after year—and it still looks great.

The off-the-shoulder top is one such style. The top was huge in the 70’s, made a major comeback last year—and now, with summer around the corner, the demand for this style is even stronger. Off-the-shoulder tops, especially those with sleeves, are cute (and comfortable!). Plus, they look good on almost every body type! Luckily, right now there are so many cool options to choose from.

Whether it be a solid cropped piece or an long sleeve ruffled top, I’ve picked a few of my favorite styles—shop them below!

First things first: It’s been a powerful year for women everywhere. Let’s look back — starting from the historic women’s March to the women bravely naming their harassers (and the women supporting these women) and the women (and men) wearing all-black in solidarity with anyone who came forward with sexual harassment and assault allegations in Hollywood and elsewhere — Yes, a lot of progress has been made.

But.

But a lot remains to be done to support women’s rights around the world. Despite gender equality initiatives to break glass ceilings, men are still paid more than women (but sigh, right?). You know it: we’re talking about the pay equity gap. It’s fact: women have a money problem. And that problem is that we earn only 77 cents of each dollar a man makes (double sigh.). Less if we work in certain industries, and even less if we are women of color.

This number portrays a macro view of the gender pay gap and is subject to many factors outside of gender, such as age, experience level, and industry. The pay gap has been researched and debated for decades, with little real progress to show for it — Men are still being paid much more than women, and their earnings are increasing more rapidly. This means the pay gap is widening.

This is a problem, no doubt about it. It’s unjust. And we should fix it. But, that’s not even the start of what we’re dealing with here, and we shouldn’t fall into the conventional view that the pay gap is the only money issue facing women. So, if we’re going to talk about the gender pay gap, we need to talk about all the other gender gaps facing women today, and how they affect our discussions of what equality looks like.

Contrary to popular belief, the gender gap is not as simple as saying that men and women doing the same job are paid differently (although that is part of the story too). Women also have less money partly because women are more likely to work in industries with lower average pay, they are more likely to undertake part-time work, due to commitments to care for either children, elderly parents, or both, and they invest less than men.

Wall Street veteran Sallie Krawcheck is making closing the investment gap her mission with digital investment startup Ellevest. “Wall Street has failed to serve women investors,” Krawcheck says, noting that many financial institutions have been unsuccessful in their attempts to draw in women. “It’s important because it’s important for our economy and society,” says Krawcheck of getting women to invest at the same level as men. “When women are financially stronger, it’s not just good for them, it’s good for their families, it puts money into the economy, the market — it’s good for everyone.”That’s not an opinion. The Pew Research Research found that an increase in the percentage of women participating in the U.S. workforce was instrumental in raising the standard of living between 1950 and 2000. According to a McKinsey study, one-quarter of the U.S.’s current GDP since 1970 can be attributed to having more women in the workforce.

“What’s even crazier is that women have such a big and positive impact on the economy despite dealing with gender gaps that both hinder our ability to truly unlock our potential and cost us significant amounts of money over our lifetimes,” says Krawcheck.

This is by no means meant to suggest that the stock market only goes up. But historically — counting up years, down years, and bumps along the way — the stock market has returned 9.5% on average annually since 1928. This is quite a bit more than keeping the money in the bank these days, where it can earn close to 0%. Historically, the reward for weathering some market ups and downs has been well worth it. So, how much are we talking about here?

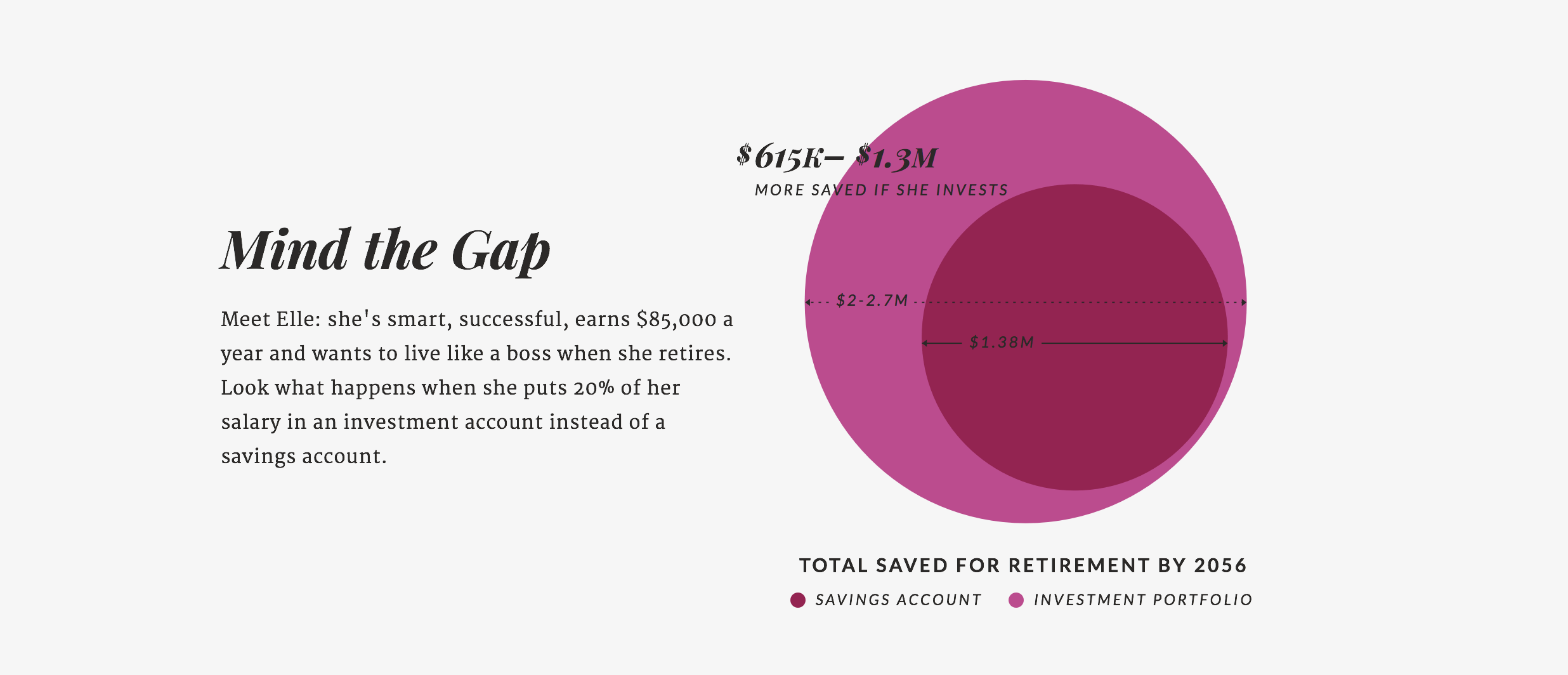

Get the glass of wine ready, it’s a doozy. Starting with the pay gap, the numbers look like this: Let’s say you’re making a salary of $85,000 a year, and you have 40 years left to work ahead of you. Hypothetically, let’s say you get the raise to the guy’s level, and you’ll earn an additional $1 million. Good for you. But, wait. . . What if you take 20% of your (pre-raise) salary and invest it in a diversified investment portfolio — one made up of stocks and bonds — rather than leaving that money in cash? Over the next 40 years, Ellevest estimates you’ll earn an additional $500,000 to $2.1 million, depending on market performance.

An extra $1 million in increased salary is good. An extra $500,000 to $2.1 million is also pretty good.

So, why are we all fixed on the idea that the raise will make us more money?

Don’t get me wrong, the gender pay gap is a real problem that needs a real solution. However, the pay gap should be even more reason women should invest — because we should be making the most of every penny. It’s because of the power of compounding. Albert Einstein is to have called compound interest “the most powerful force in the universe.” Compounding essentially means that you earn returns on the money you invest. . . and over time, you also earn returns on the returns themselves.

Need some clarification? We got you — Here’s an example from Ellevest: Let’s say you invest $1,000 and the market goes up 10%. You’ve just earned $100. If the market goes up another 10%, you earn that 10% return on the original $1,000 and on the $100 you just earned. So that same 10% market increase means you earn $110. Do this again. And again. And over a long enough period, it’s game-changing, aka, it really really matters.

When’s the right time to take your money out of the bank and invest?

“The right time to take your money out of the bank and invest is almost always “now,” so that the power of compounding can begin to work its “magic,” says Krawcheck. You should — without a doubt — ask for the raise at work but if you want to make the most of that paycheck: INVEST IT.

And if we strike out on the raise? It’s OK — But it doesn’t mean we should throw our hands up on investing, thinking that we will somehow make more money later and invest then. Instead, let’s take financial control now — because the earlier you start, the better.

Wondering how much to invest? Krawcheck advises you invest a flat percentage of your paycheck. She also suggests 50% of your income should be allotted to your needs; 30% to fun; and 20% to future you. More on how to divvy up your paycheck for financial success.

You’re not alone if you’ve ever asked yourself, How does investing work? It’s an area of adulthood that can sound intimidating if you’re new to the game, but one that is necessary if you want to build your wealth.

Enter Priya Malani, an entrepreneur and founding partner at Stash Wealth, a financial planning firm for H.E.N.R.Y.s™ [High Earners, Not Rich Yet]. Ahead, she’ll explain why we need to move past our fear, get educated, and start investing so we can work towards our goals. It turns out it’s not as complicated a topic to understand as it may seem — and the earlier you start, the better.

When I talk to women (and men) I typically hear something along the lines of “I work really hard for my money. I’m afraid to invest it because I don’t want to lose it”. Can’t argue with that.

“In my experience of over a decade in the industry, the bridge between fear and confidence is education.”

If you’ve ever had this thought, you’re not alone — not by a long shot. A recent study by SoFi and Levo shows that a good majority of Millennial women have extra money each month, after paying bills but aren’t investing for the reason above: fear.

The unfortunate part about that this is, women are making more money and are more powerful than ever before, but we are still behind when it comes to investing and financial planning.

But the fear isn’t just related to losing money. It’s related to other things like not knowing how and where to start, the indecipherable jargon, the seemingly complex strategies it takes to invest well, and simply not knowing the right questions to ask.

As a financial professional, I have personal beef with the male-dominated wealth management industry because it has historically kept women from achieving their financial goals — which is partly to blame for perpetuating the fear-factor. The industry has no interest in educating us about investing.

So most of us put it off, not knowing where to turn, and failing to consider the repercussions of not investing . . . when, in fact, investing doesn’t have to be that complicated.

Here are the most common reasons women aren’t investing and why you should start.

The excuses for not investing

1. This sh*t isn’t taught in school

I find it surprising that no matter what profession we choose, understanding how to be smart with our money is essential, yet, it’s the one subject not taught in school. We learn Spanish, French, etc. But in order to adult, we need to speak the language of money.

I’m confident that the internet is both the best and worst thing to happen to us. When most people research how to invest, they end up in a black hole of obscurity. There is no clear-cut answer on how and where to get started.

Unfortunately, because of inflation (the cost of things getting more expensive each year) money in the bank is as good as keeping it under a mattress. Over the long run, you’re actually losing around 3% off your money each year by keeping it in savings and not investing it. That’s not a great deal, IMO.

So investing is not your enemy. In fact, it’s your greatest ally in making your money work as hard as you do and it’s vital if you want to turn your hard-earned income into real wealth.

But the #1 reason women should invest is that contrary to popular belief, research shows that we are actually pretty good at it – better than men even. That’s right — according to data from financial services firm Fidelity Investments, women are actually superior investors. In analyzing more than 8 million investment accounts, Fidelity discovered that women not only save more than men, 0.4 percent, their investments earn more annually, also 0.4 percent.

It’s time to level the playing field for women. Together. Here’s how we do it. You in?

At the core, impact investing is designed to effect positive social and economic change. At Ellevest, this is done through impact investment portfolios that work to advance women. With these, you could earn a competitive return so that you can reach our goals — like starting a business, buying a home, starting a family, and retiring comfortably — by investing in other women (brilliant, right?).

3 REASONS WHY WOMEN ARE GREAT AT INVESTING

1. We are less likely to react

The biggest mistake the average investor makes is to get emotional about short-term movements in the market. When you’re investing, you want to keep emotions out of the equation and remember that investing works over time not overnight.

2. We buy right and sit tight

A few years back, Fidelity did a study of all their client accounts and found that the 401(k) seemed to be the best performing account for the average person. The reason why….because most of us forget our password! Crazy, right? But it’s true.

3. We tend to be better at delayed gratification

One of my all-time favorite quotes is: “all long-term investors want short-term results”. Women tend to do a better job accepting that investing takes time to work and don’t meddle with their investments nearly as much as men.

So while it may not feel like it, you’re inherently ready to invest. Time to move past our fear, get educated, and start investing so we can work towards our goals.

In a year of widespread activism, one way you can take action and fight the gender wage gap is start investing in Future You because money is power. Here’s one way you can do it: Get started with a free investment portfolio in under 10 minutes based on your finances and a gender-specific salary curve and then open an account today.

When you hear the words “successful women,” who comes to mind? Women in power suits walking down 5th avenue? Ruth Bader Ginsburg unifying a room of politicians? Beyoncé?

Today, there is no shortage of trailblazing, badass women to look up too. . . While women like RBG, Sandberg, and Beyoncé have been able to reach a point of success in different ways, there is one thing all successful woman have in common, and that is that they make their money work for them. In other words, they work smarter, not harder.

Interestingly, a recent report of the Ellevest 2018 money census revealed that the #1 thing that makes women feel in charge of their futures is “putting away money for financial goals,” followed by how much we save (#2) and how much we invest (#3). In fact, getting involved with our finances had a bigger positive impact on how in charge women feel than our educations (#8) and the support we get from our families (spouse/partner, family/parents and even being a mother or a father) (#6, #9, #10).

But, if that feels crazy or incorrect, it should, because according to a recent Fidelity report, while 92% of women want to learn more about financial planning, 80% aren’t talking about money with anyone; and only 47% feel comfortable discussing money with a professional. As a result, we lag behind men in how much we’re investing and, in the long run, how much money we’re making.

We’ve been told there’s financial stuff we should take care of when we are adults — like setting up a 401(k) or investing in an IRA or saving for a down payment for a home — but until now, many of have been happy just to do the basics and saving, and it’s hard to think about how to take our money further.

But, the truth is that while saving is great when you leave your savings in cash, it’s possible you are missing opportunities because you’re singularly focused on saving your dollars and not allowing the money to work harder for you. “This is the precursor to the gender investing gap, and it’s not our fault. Honestly, it’s not,” says Wall Street veteran Sallie Krawcheck who’s making closing the investment gap her mission with digital investment startup Ellevest.

Personally, I have also always felt like I don’t have enough financial knowledge to get started investing, and I don’t have the time to learn. But not taking care of your finances is like not taking care of your physical or mental health. Something I’ve learned from the team at Ellevest is the stuff I previously found super complicated isn’t actually that confusing. And, yeah, it takes a little time to get started. But we’re talking your money here. You need it.

So how much could you really be making if you started investing this week? I asked Krawheck to crunch some numbers, and here’s one example:

If you’re making $85,000 a year and putting 20% of your income in the bank, you’re losing out on $1.1 million or more, over the next 40 years*. Want to know what the short term of that looks like? If you’re making $85,000 a year and putting 20% in the bank, and wait 10 years to invest, you could be losing about $100 every day. For 10 years.* That’s right.

Not investing because you want certainty? If you save 10% of your income for retirement annually and put it in the bank, your chances of retiring well (ie, 90% of your pre-retirement income) for a woman’s expected lifespan is 0%. Scary? It should be.

So what’s a wanna-be-debt-free woman to do? Keep reading.

The very first thing you must do before invest is to pay down your credit card debt. Even better, pay it off entirely.

Pay down or refinance any other debt with an interest rate in the double digits.

Set up an emergency fund. This can be in your checking account, or better yet, in a separate savings account. (I don’t know about you, but the balance in my checking account tends to go down as fast as it goes up.) Three to six months of your take-home pay is a good guideline here. Why is this so high on the priority list? Because s*** happens. Because roofs cave in, because people get fired, because you might need to get a new car. Make sense?

Once you’ve gotten rid of your high-interest debt — Congrats! The rule from here on out is pay yourself first. Put away a percentage of your after-tax salary every month. . . The breakdown should look something like this: 50% for needs/30% for wants/ 20% for investing (more on the breakdown here).

Get that 401(k) match (if your company has one) by investing part of each paycheck. A match is free money; don’t leave it on the table.

Women need to have the same financial security that men do, not just for themselves, but for their families. With more and more women being the primary or larger breadwinner in the family, the money they make, save, and invest represents the future for their entire families, just as it always has for men.

With more stay-at-home dads than ever before, women represent a larger part of the workforce than ever before in recorded history, which means they need that larger slice of the pie to save and to create more wealth from through investing intelligently, Ellevest helps women do this through listening to women to understand their needs, and by offering them 401(k)s, IRAs, and other saving and investing tools that are tailored to their unique needs.

Money Makes Women Feel In Control

It’s not just a matter of saving and waiting for tomorrow — Ellevest knows that a lot of how we feel about today and our overall lot in life has to do with how we feel, whether or not we feel safe, and whether we feel like we could weather a tough storm if we didn’t have work to count on for several months. The truth is, most of today’s women and the families that depend on their income will not be financially secure if that woman loses her job and cannot find work again right away. Money makes the world go round, but it also makes us feel safer, better, healthier, happier, and like we can face an uncertain future ahead.

And, that’s exactly why 63 percent of women surveyed by Ellevest said that money made them feel in charge of their lives.

Want to own your own home? Start your own business? Make that big splurge that you daydream about? What are the chances of achieving them if you’re just dreaming about them? Pretty low. Research indicates that your chances increase if you just write your goals down. Then you can plan for and invest in them.

At Ellevest, they build each personalized investment portfolio with a target of getting you to your goal, or better, in the significant majority of markets. That’s a lot better than dreaming.

“Too many people spend money they earned, to buy things they don’t want, to impress people that they don’t like.” ― Will Rogers

I talk a lot about the global investment markets here. I’m focused on making profits, and often I’m looking to make multiples, knowing full well that some opportunities won’t work out. I’ll get the timing wrong or I’ll miss something entirely and need to hedge, reposition, or exit entirely. That’s life.

But I haven’t spent much time on stating the obvious (because I figured it’s obvious) so in this post, I’m going just that.

We are going to forget all about economics, financial markets, central banks, derivatives, GDP, and all that fun stuff, and we’re going to go all the way back to some basics.

Basics which purple-haired grandmothers everywhere would approve of as they make that second cup of tea from the same teabag. I am writing this because I receive emails from people of all ages looking for advice. From middle-aged guys and gals asking, “What do I do now to get secure?” Secure… not rich, just secure.

Why? Because they’ve been making the wrong decisions for at least two decades and they’re just now realizing time is running out and the current path of mediocrity isn’t likely to make them rich, let alone secure. That’s a big problem, which I’m not even going to try tackle here.

This article is for those women who haven’t yet been led down the rosy path of consumer-driven expectations. The goal here is to build net worth as fast as you possibly can.

So, what exactly is net worth? Is it the amount of accumulated wealth you own?

Nope, not really. That’s a terrible metric. Net worth should really be calculated as a number of years, not a dollar number. I call it the “the beach ratio”. Net worth is the number of years you can sit on the beach doing “sweet FA”. If you’re tracking your net worth, you can see the progress you’re making toward your financial goals. It can also serve as a warning if you’re not meeting goals so you can then adjust and adapt your financial plans as needed.

Speaking of goals, your goal should be to ensure you don’t end up like this:

The above data comes from this study done by the Economic Policy Institute. A couple of things to consider: the average American couple (that’s two working people!) has $5,000 saved for retirement (yes, really). Nearly 40% of the population has only $480 saved. Now, how many of that same 40% own a new smartphone? Just sayin’…

Along with wage inequality, women retire with just two-thirds the money men have, all while living at least five years longer than men. “As women, we have a number of money gaps. We don’t invest as much as men do…we don’t make the money men do, we aren’t as advanced at work as men, things actually cost us more, [and] we have a gender debt gap,” Krawcheck told CNBC’s “On the Money” in an interview.

“We’re not going to be equal until we’re financially equal,” said Krawcheck, a Columbia Business School graduate, and a veteran of banking giants Bank of America and Citigroup. To help close the financial gap, Krawcheck realized women’s needs and goals needed to be addressed in a better way. It’s one she started Ellevest.

Keep reading for my top four financial lessons every woman needs to nail.

1. Set Yourself a Base FIXED Expense Ratio

Let’s get practical…

Let’s say you come out of college or high school and you’re earning $50k/year. For goodness sake don’t spend more than 10% of your income on accommodation. Now immediately I know I’m going to get a ton of emails saying… “Oh, but you don’t understand Chris…where I live you can’t get a decent apartment for 3x that.”

Look. You have to decide if you’re prepared to sell your future upfront for comfort now or not.

When you’re in your 20s you can (and absolutely should) flat-share with others to ensure that you don’t castrate yourself financially before you’ve even tried to procreate. I know of people spending 30% or more of their income on rent and doing it well into their 30s, 40s, and even 50s.

That, my friends, is catastrophic to wealth creation and is like dumping a bag of cement on your back and then trying to swim the English Channel. Good luck, you’re cementing your path to poverty. Real poverty, like in those 3rd world charity commercials you’ve seen, because for anyone that’s been reading capitalist exploits for some time they are fully aware there is a coming pension crisis and there ain’t nobody to bail you out but you.

The task is to fix your expenses as low as you possibly can and then work your tail off on expanding the right-hand side of the ledger.

As a rule of thumb, your expenses should never exceed 70% of your net income, though 50% is really the number. (more on that here.)

When you’re in your 20s it means no $7 tequila shots to be had from the gyrating crotch of an intoxicating beauty and no lattes to follow the morning after to cure a hangover.

You won’t have the time. All your time should be focused on generating income streams. If you don’t like the concept then, by all means, join the rest of the crowd, enjoy yourself now and welcome a life of mediocrity. Nobody will fault you for it because it’s what everyone does. This is your choice. It’s black and white. You’re in your 20s—you have high energy levels, don’t need much sleep, have high-risk tolerance, and now is the time you actually should.

This should be at least three months of take-home pay, in case you get fired (hey, it happens—more than any of us like to think), or in case you have to take time away from work for, you know, an emergency. That money should be held in cash, for safety. Ellevest is working to close the gender investing gap, so they don’t charge anything for those and you should have that set aside before you invest. Sign up right here.

And the next step is… begin to invest for retirement, and invest for other goals.

“When it comes to investing, pay yourself first. Put away a percentage of your after-tax salary every month. The breakdown should look something like this: 50% for needs, 30% for wants, 20% for investing,” says Krawcheck. It’s recommended that you do this after building an emergency fund—and not until you’ve paid off your high-interest debt.

What should you invest in?

Retirement: Get that 401(k) match (if your company has one) by investing part of each paycheck. A match is free money; don’t leave it on the table—do what is necessary and do it early. If you’re working as hard as you should be at this age you won’t have the time or energy to be spending any money anyway.

2. Increase Revenue

Let’s say that in year one your base salary was $50,000, you spent 70% on expenses ($35,000) and therefore by default saved $15,000.

For the purposes of this article let’s work on a 3% annual pay increase. You’ll be gaining experience, increasing your skill set and this is reasonable. It can easily be higher but let’s be conservative. Your base expenses remain and your net worth has gone from $15,000 in year one to $31,500 in year two ($15,000 x 2 years + 3% on $50,000).

Realise that in year two you’ve increased your net worth generated for that year by 10% and you’ve more than doubled your net worth because you’ve got your expenses fixed.

My readers are a sharp bunch so you’ll understand quite quickly that if you get more than 3% pay increase it all drops to the bottom line.

3. Rethinking Risk

As mentioned in point 1 above you should be taking risks. What sort of risks?

Risk your time on things that will educate you to be able to execute better. Develop skills that you can monetize.

If you’re in a job, which presumably you are or will be, you should be on a constant lookout for opportunities to try your hand at building business incomes. By the time you’ve been at your job for 3 years if you’ve not got at least one side business operating outside of your job, you’re doing it wrong.

Take on too little risk (such as with an Emergency Fund), and your money doesn’t grow. Take on too much risk and you may earn a higher return over time, but you can also experience more significant market ups and downs. And, you might end up needing your money at an inopportune time in the markets.

Hmmm.

According to Krawcheck, based on the hundreds of hours of research they did with women like you, targeting that 70% probability gives you (and them) enough confidence that we can all sleep at night, but gives you the opportunity to grow your money in a way that is simply not possible at 100% probability.

And at Ellevest, they don’t just set your “risk budget” and go the beach: they make sure that the 70% probability stays at 70%. Because things happen: markets go up, markets come down, you may not make a monthly deposit, time passes. Accordingly, they employ their proprietary technology to monitor your investment portfolio on a daily basis—to keep it at that 70%, and they adjust it as time passes (and your investing time horizon shortens) into lower-risk portfolios. Ellevest believes that investing this way increases the chances of your reaching your goals, substantially, as you move from dreaming about something to articulating your goal, to investing towards it.

After you figure out what you need to do to achieve your goals, figure out how to automate it. You can set up a recurring contribution on Ellevest and change it at any time. There’s no commitment. By and large, financial advisors charge fees of about 1% to 2% of your assets. In the case of Ellevest, however, the fees are just 0.5%. (Ellevest can charge low fees because it uses a lot of low-cost exchange-traded funds.)

4. Add Additional Revenue Streams and Buy “Long Dated Options”

Your income is going to be rising because you’ll be working your little tail off in your job, and additional gigs which bring income.

Let me say one thing about taking additional gigs to earn more income. Focus on things which increase your skill sets. (some examples) Pumping gas won’t do that, waiting tables won’t do that. Instead, pick industries that are evolving where opportunities will open up… if only due to fewer entrants knowing they exist. Robotics, programming, anything that can’t be automated away because automated away it will be. It’s only a matter of time.

If you ever attend those bars and clubs your peers are going to on weekends it should be to learn and work in the clubs. If you get lucky on the side all the better but you’re not focussed on that. Learn the mechanics of the business. When is the club owner looking for that $250k expansion capital to set up a new club across town guess who’ll have the investment capital to take an equity ownership, and have a deeper understanding of the business?

Buy long-dated options.What do I mean by this? Let me use an example: In the early and mid 2,000s, I had some friends who were earning great money doing web development. Some were taking additional courses to better their skill sets but there were no barriers to entry. None. Ok, there was the MCSP (Microsoft Certified Systems Programmer). Remember that?

One friend saw the writing on the wall for his job and continued to work in his job but instead of “up-skilling” with various programs sold, used his spare time to moonlight at a firm building CMS systems. The skills he picked up there helped him snatch a job which included an options package at a Danish software development company which went onto developing a CMS system for packaging firms and after just 7 years and a buyout from a private equity firm he walked away with about 14 million euros.

What You’ll Get: When you internalize what I’ve just said and really get it. You’ll see a marked change in your net worth in just 2 short years and you’ll realize that every single dollar you SPEND is arsenic to your net worth (beach years). Stick with it and you’ll get income acceleration as you have increased not just income but most importantly net worth.

This is pretty much guaranteed if you stick to it. By the time you’re clocking in at 30 years, you’ll be wealthier than most highly paid investment bankers (trust me on this) based on how many years you can survive (remember: the beach ratio).

Remember, it doesn’t matter if you’re earning $100,000 a year or $1 million a year. What matters is how much you’re spending relative to your income which provides you with your “beach ratio”.

Your living standard can increase but NOT at the expense of your “beach ratio.” Preferably this is always accelerating meaning you can outlive your money at which point a rise in your living standard won’t affect your security.

Ready to invest? Ellevest has no minimum so you can start investing with as little, or as much as you like.

Adapted from Capitalist Exploits, by Chris MacIntosh, fund manager, and adviser. See the original story here.

Here’s the thing about women: We’re patient. Maybe it’s genetic. Maybe it’s because we’re used to waiting for what we want. Maybe it’s because we realize that good things take time to become great — whatever the reason, when it comes to investing, patience is a significant advantage.

In fact, there is no reason why more women aren’t wealthier. By most accounts, women control somewhere between 30% and 40% of global wealth. That’s not shabby, but it’s fairly low considering that women are natural investors. We’re well educated (in the U.S., we’re more likely to go to college and graduate from college than men); and we’re good at saving money (better than our male counterparts); and when it comes to investing, we commit to a plan better than men, and we’re less likely to move our money around in market fluctuations, which can be a very expensive habit.

By contrast, men are notoriously trigger happy and overconfident as investors; they lack patience and expect immediate returns. According to one study, men traded 45% more than women, and all that trading reduced men’s returns by 2.65% a year, up sharply over the 1.72% in reduced returns women saw from excessive trading. Women’s greater patience sounding more convincing now?

So, If Women Are Such Great Investors, Why Don’t More Women Do It?

In part, it’s because the financial services sector (i.e. money managers, investment banks and retail banks) has long overlooked and neglected its female customers. A damning report from the Boston Consulting Group a few years back, for example, showed that women were very unhappy with the financial services they received. Of those surveyed, 55% felt that wealth managers could do a better job of meeting women’s needs; and 24% thought that private banks could significantly improve how they serve women. The problem, they said, was that men got more attention, better advice and even better terms on deals. (Not to mention, some women found banks’ “pink” marketing campaigns condescending and insulting.)

As one woman surveyed said, “What banks need is a revolution like the automotive industry had: to finally understand that women not only sit in the cars but also choose, buy and drive them.” Some businesses have caught on.

Case in point: Ellevest, a revolutionary women’s investment platform started by Sallie Krawcheck, former Citigroup CFO and longtime Wall Street exec. The goal of Ellevest is to close the gender investing gap.

Krawcheck says the idea for the business came to her after an a-ha moment when she realized that the investing industry — a by-men-for-men business — was systemically keeping women from meeting their financial goals. It’s a particularly painful problem given that women’s financial needs are very different from men — they tend to be disproportionately affected by life events (having children, divorce, losing a spouse, and so on) and earn, on average, less money than men. Because of these reasons and more women need to invest their money early so they can benefit from compounding. But, how and where do you start, you may ask?

All About Your Goals

Sometimes, a starting point can really come in handy. Think back to when you first applied to college. The whole idea of applying and getting in, visiting schools, packing for school, and graduating was all daunting, but it all started with a plan. You needed a plan and goals set in place to succeed; investing is no different. When it comes to investing like a woman, Ellevest can help you take the guesswork out of the investing and help you invest in your biggest goals.

But that’s just the beginning. Customization matters a lot at Ellevest too: They customize each of your investment portfolios to each of your goals, and they customize your financial plan to you. Which is why they’ve also given you the ability to customize your goal targets, your timeline for achieving them, and the rhythm with which you invest your money to get to your goals.

Disclosures: We’re excited to be teaming up with Ellevest to start this conversation about women and money. We receive compensation if you become an Ellevest client.

Establishing good habits in life — and I mean, really establishing — is one of the best things a woman can do for herself.

Third month into 2018, I find myself getting addicted to good habits — hanging up my clothes as soon as I get home, paying bills during the second day of every month, making plans and committing to them, even when I feel like canceling (nobody wants to be that friend!) Good habits take some work in the beginning but always pays off because they are what make you efficient, successful, and if you stick with me for the next few paragraphs – wealthy.

Keep reading for the #1 money habits of successful women.

Successful women who earn more money share this one habit – investing.

Here’s the thing: Today, women in the United States control over $5 trillion in investable assets, and the potential for future growth is enormous. Considering this figure, you’d think that we women would be set up well for retirement. But, the sad fact is we’re not — and the guys are (SIGH) — and this is simply because the guys are investing their money and we’re not.

Despite all the advances we have made in the workplaces, we still lag behind our male counterparts when it comes to retirement and money. On average, men’s retirement account balances are more than 50 percent higher than women’s and this further compounded by the fact that we tend to live an estimated five to six years longer than men. This means we not only earn less, [but] we also need those assets last longer. Given these statistics, it’s critical that we ask not only why this gender retirement gap exists, but also what we can do about it.

Currently, there are almost 75 million of us in the U.S. workforce; we’re educated, earning money than we ever have and starting our own businesses. Yet with all of the discussion around women’s issues, there is one area that has received little attention — and which can have a big impact on our lives — is the gender investing gap.

“The good news: we can fix this,” says former Wall Street executive-turned entrepreneur Sallie Krawcheck, the CEO of women-led digital investing platform Ellevest. Krawcheck has a plan to finally put women on a level playing field with men. “Money is power. Money evens the playing field for us as women. Money is knowledge. Money is confidence. Money is freedom. Money is, ‘Take this job and shove it,’” Krawcheck says.

Successful women know that Investing their money — when done right — is one of the best ways to make their money work for them, and it’s absolutely critical for retiring comfortably. No matter what age you are, if you’ve paid off credit card debt, and put a little bit aside for rainy day fund, it’s time to start investing a percent of your paycheck each month.

For a professional woman, putting away paychecks into a savings account and not investing that cash can translate into hundreds of thousands or even millions of dollars lost over the course of a lifetime. A dollar invested in your 20s is worth so much more than a dollar invested in your 60s. So start today.

But what about strategy? Timing? All those things I need to “beat the market”?

It’s not about how much you can invest right now, it’s about starting the habit with a percentage, any percentage, of your monthly salary. Even though the ultimate goal is to put away twenty percent of your monthly payment toward the investment of your choice, this is really about building a habit, so even starting at 1% or 5% will go a long way. And just like starting off every Monday morning with your fridge stocked and laundry done, the next stage of your financial future will be effortless so you can focus on other things – like asking for that next pay raise.

Allow me to introduce you to a really sexy term: compound interest. Compound interest is the addition of interest to the principal sum of a loan or deposit, or in other words, interest on interest. For example, if you make $85,000 annually and put away the recommended 20% savings and invest it in a diversified investment portfolio instead of leaving it in the bank, Ellevest estimates that you would have an additional $565,000 to $2.1 million more, depending on markets. So, on average, let’s say $1.4 million more. This is the result of reinvesting interest, rather than paying it out, so that interest in the next period is then earned on the principal sum plus previously accumulated interest. Talk about really strategic retirement planning! Letting your money really work for you instead of sitting and building up the bare minimum interest.

Disclosures: We’re excited to be working with Ellevest to start this conversation about women and money. We receive compensation if you become an Ellevest client.

International Women’s Day is an incredible day for every woman. It’s a day where we give homage to what women all over the world have done in pursuit of equal rights and it’s a time to come together as women to celebrate each other. It’s a day full of celebration for and by women, whether you’re celebrating in the U.S. or abroad, with family or with friends.

At Style Salute HQ, we’re all about celebrating and supporting women.

And in honor of International Women’s Day, we are kicking off a new series called Make a Power Move, where we will share all the ways women are leaning into their ambitions. These stories are meant to provide an inspirational forum for women everywhere to champion one another other and truly — truly, truly — become their best selves.

IWD is also a reminder of how much we have left to do to achieve equality. While we have made incredible progress in the ways of equality, we’ve still had a long ways to go on issues like the gender pay gap and paid family leave. Want to know more about the issues and what you can do to pursue progress? You’re in luck. Ahead, we’ve put together everything you need to know about IWD. So, go ahead and bookmark this page and share the information with your friends and family, and on March 8, get ready to celebrate the women in your life.

What exactly is International Women’s Day?

IWD is a celebration defined as a day “celebrating the social, economic, cultural and political achievements of women” and is currently celebrated in over 100 countries throughout the world as well as an official holiday in more than two dozen nations including Afghanistan, Cuba, Georgia, Laos, Russia, Uganda, and Vietnam. Because we are ever-changing, there are different goals every year. For 2018, we are pressing for progress to motivate and unite friends, colleagues, and communities to think, act, and be gender inclusive. Start the discussion with your community about getting IWD in the classroom, challenge women’s equality in sports, and celebrate the programs that promote advancement for women in STEM.

When did International Women’s Day get its start?

The concept of International Women’s Day (IWD) can be traced as far back as 1909, gradually gaining momentum the following years as the celebration became a political instrument for expanding women’s rights. It started with the right to vote then evolved into so much more – the right to hold public office; the right to be employed without sex discrimination. We owe a lot to our sisters for across America, Europe, and Asia for starting this revolution and forming our socio-political culture to the ripe grounds for discussion it is today.

How do we celebrate International Women’s Day?

From tokens of appreciation (notes and flowers from both genders to the beloved women in their lives) to organized rallies, the principles of this holiday remains the same: Be fearless and stand up to what’s right and equal to #MakeaPowerMove. We cannot think of better ways to encourage power moves at Style Salute than promoting equality in the home and workplace through knowledge and smart financial planning.From closing that gender pay gap to knowing when to invest, we are here to guide you toward financial freedom on this important day.

What can we do to break the Gender Gaps on International Women’s Day

Gender equality and addressing all the gaps (both money and physical boundaries) are in the spotlight like never before. With knowledge comes action and now is the time to really power forward to make a difference in your financial future. We cannot emphasize enough that gender equality is a 360 degree approach that encompasses assertiveness with money, workforce, colleagues, and community at large. Let’s start with the greatest gap we see – the pay gap.

Money is power and this power has been woefully unequal ever since the dawn of the workforce. We know what workplace equality looks like, and it’s a bright world of wealth and progress – According to a recent McKinsey Report, full gender equality could add up to an estimated $4.3 trillion to the U.S. annual GDP by 2025. That would bring our projected GDP up to $26.3 trillion.

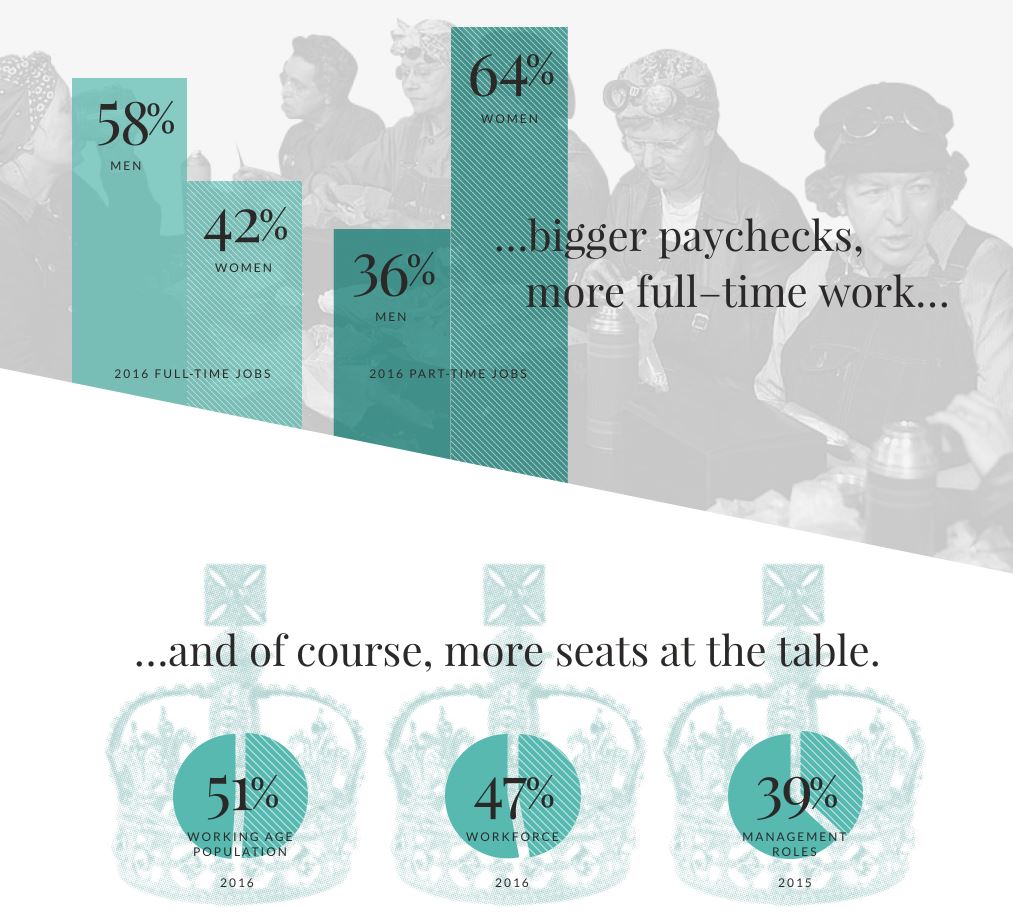

Sally Krawcheck, CEO of Ellevest, has done significant research into the work it would take to reach full gender equality. Surprising news to none, there is a still a long way to go to address the pay gap, female underrepresentation — in full-time jobs, high-paying industries, management-level jobs, and the workforce overall — and the reality that women handle the bulk of the unpaid labor.

Yes, we may hold 47% of the workforce, but we also hold only 43% of full-time positions and 64% of part-time roles. In 2015, only 39% of management positions were held by women. Only a few more statistics into the urgency of this issue, I promise – women are only making 75-80% of the salaries men earn for the same jobs and this pay gap only continues to widen as women ask for fewer promotions and invest less than men. A lower percentage of us have started saving for retirement than men, we have saved less, and we park 68% of our money in cash, not investments that could pay off so much greater over time.

So what is your story? Have you been able to start a business of your own or begin a habit of investing to be able to seed that start-up? Have you elected to spend money at women-owned or women-celebrated establishments only to make your dollar count? Or have you decided to unleash your power to capture your share of the billions of dollars in potential wealth at your fingertips by investing? Our dedicated writers and readers have inspired us with their tips and strategies on making it happen, as we hope it motivates you as well.

We want to hear it all and follow you on your journey. If you need some guidance on how to start financial planning for your future, Ellevest offers a free plan to start you on your way toward smarter wealth management. Take a stand for your own finances —Ask for a promotion. Start investing. Get your own finances in order.

This International Women’s Day, all of us here at Style Salute wait for your #MakeaPowerMove story and empower you to take what’s your today and tomorrow.

Disclosures: We’re excited to be working with Ellevest to start this conversation about women and money. We receive compensation if you become an Ellevest client.

Your closet called, and it needs some spring dresses and boots. We’ve rounded up the best spring dresses and boots to take you into spring in seamless style.