Build your dream summer beauty bag with these with time-saving skincare, makeup, and hair products that are perfect for summer.

Why a Prenuptial Agreement May Be a Smart Option for Women

Long before you pop the “M” word, you should pop the “P” word.

As a result of the high divorce rate, changing divorce laws, the trend toward marrying later and great longevity, the number of prenuptial agreements has increased exponentially. A prenuptial agreement (A.K.A. a prenup, premarital, or antenuptial agreement) is an agreement between two people who are planning to marry.

The idea of bringing up a prenuptial agreement, however, still makes many people uncomfortable. Many people carry preconceived notions and baggage about prenups. “Isn’t my future spouse going to be offended?” Maybe, yes – but, it’s necessary to bring it up.

While prenups have received a lot of public and media attention recently, many people still don’t understand their value or how to broach the subject.

Why Get a Prenup?

Why? Bringing up the subject of a prenuptial agreement can be a great way to learn more about one another’s expectations, dreams, and hopes. In fact, more women than ever are instigating prenuptial agreements to protect their assets. Many women today earn a substantial income and have amassed assets of considerable value.

You may have a pension plan, investments, and bank accounts. You may be earning, or anticipate earning, a lot of money and want to retain the right to do what you want with that income after you marry. Whether you have a high net worth or are just starting out, have children or don’t, there are dozens of reasons a prenup is beneficial to you and your future spouse. Here are just a few:

- To protect your pre-marriage nest egg (such as your home, pension plan, stock portfolio, or property with sentimental value) To protect gifts and inheritances you receive

- To ensure that in the event of death or divorce, you will avoid difficult disputes over property (such as family businesses, stock options, professional degrees, licenses and practices, pension plans, and copyrights)

- To ensure that children from a prior marriage receive their intended inheritance

- To insulate ownership in a professional practice or business

- To protect yourself from your partner’s pre-marriage debt, e.g., credit card debt or student loans

- To establish the value of non-monetary contributions to a marriage, such as being a stay-at-home spouse and making career sacrifices

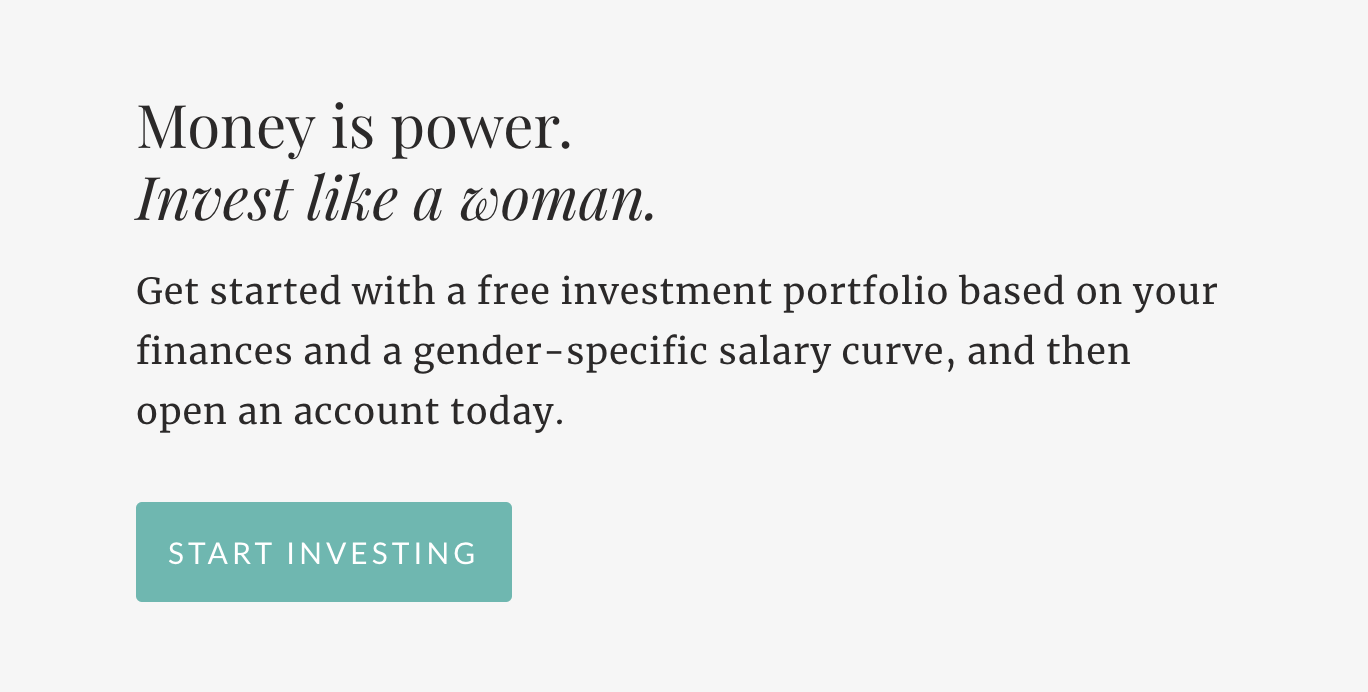

Why Women Should Have Their Own Investments

Investing is a skill every woman should possess. At some point in our lives, 90 percent of women will be single, divorced or widowed, according to the U.S. Bureau of Labor Statistics, and therefore entirely responsible for our finances.

Yet, still, many of us either don’t invest or delegate the task to someone else, be it a spouse or a financial advisor. According to Ellevest, a digital investment platform for women, taking positive action with money is a huge confidence booster for women. Recent data also showed the #1 thing that makes women feel in charge of their futures is “putting away money for financial goals,” followed by how much we save (#2) and how much we invest (#3).

In fact, getting involved with our finances had a bigger positive impact on how in charge women feel, more than how much education we had (#8) and the support we get from our families (spouse/partner, family/parents and even being a mother or a father) (#6, #9, #10).

What many women fail to consider is that we earn less than men, so investing is a way to get even and catch-up. And, since we tend to live longer than men, that money from investing will really come in handy.

Ready to invest? Ellevest has no minimum so you can start investing with as little, or as much as you like.

When?

Sliding a prenup across the dinner table a week before the wedding is not the appropriate time to bring up this important topic. Conversations about concerns, expectations, and responsibilities are best conducted early in the relationship while dating. As your relationship gets more serious, your conversations should get more detailed and specific.

Where?

Where do you normally discuss topics important to your partnership, such as life goals, finances or family? Find or create a calm, neutral spot where you will both feel open, at ease and unpressured. Whether you’re sitting at your living room sofa, taking an afternoon walk or having a quiet dinner, you’ll want to create an environment where both of you are most comfortable — mentally and physically.

How?

Even when couples understand the reasons for marriage contracts, many aren’t sure just how to initiate the discussion. Here are some suggestions to get you started:

- Be open, honest and direct

- State your specific concerns

- Present an idea to be implemented by the two of you over time

- Invite discussion about any underlying issues that arise

- Work out your issues collaboratively

Conversation starters – some possibilities

“Let’s talk about our future, what we both want, our lifestyles, our present, and future finances. I want to make sure all our money issues are addressed and resolved in an agreement. Then we won’t have them hanging over us when we get married.”

“My children are very concerned about my marriage and what it might mean for their inheritance. I’m worried about this too. Since most of my assets are from their father, they are entitled to those assets. They will be happier about this marriage if we do some estate planning. That will make me happier too.”

“I worked very hard to acquire a nest egg, and I want to make sure I have it in the unlikely event the unthinkable occurs between us.”

- Prenup No-no’s

- Presenting the idea of a prenup as a fait accompli

- Springing a prenup upon your intended at the last moment

- Being overbearing or heavy-handed

REMEMBER: Don’t let a prenup fall to the bottom of your “To Do” list. The longer you wait, the harder it will become. The discussions you have revolving around the prenup are conversations you will have once you are married. Getting to know your partner’s position on these important aspects early can help head off more difficult discussions during the marriage. If you can’t talk about touchy issues during courtship, it doesn’t bode well for the marriage.

Arlene G. Dubin is a partner in the law firm of Moses & Singer LLP in New York City and author of “Prenups for Lovers: A Romantic Guide to Prenuptial Agreements.”

Here’s Why You’re Going to Fall In Love with Crazy Rich Asians

Raise your hand if you read Crazy Rich Asians in one night. Yup—that’s just about everyone that read even one page, and pretty much the reason why there’s so much excitement around the movie.

Based on the 2013 novel by Kevin Kwan, Crazy Rich Asians follows Rachel Chu (Constance Wu) as she travels with her devastatingly handsome boyfriend, Nick Young (Henry Golding), to meet his family in Singapore and attend the wedding of Nick’s best friend. The twist? Rachel gets more than she bargains for when she learns Nick’s family is essentially Singaporean royalty—they’re incredibly wealthy, and Nick is like “the Asian bachelor,” as Rachel’s close friend Peik Lin (Awkwafina) puts it:

They are not just rich, they are crazy rich, and they are ready to pounce all over our unsuspecting protagonist.

All eyes are on Rachel as she navigates this foreign land and society. What will she do? Say? Wear?

Everything that makes Rachel a confident and successful woman Stateside is turned on its head when she goes Gap espadrille wedge encased toe-to-Saint Laurent Kate satin sheathed toe with her boyfriend’s mother, Eleanor Young. Along the way, Rachel learns more than she ever expected about her boyfriend, Nick Young, and leans on college bestie Peik Lin Goh, as she discovers what she is truly made out of.

So, what’s the deal? Why have you been hearing about it so much? Besides, being a great film with an outstanding cast, Crazy Rich Asians is also the first major studio film with an all-Asian cast since Joy Luck Club made its way to screens 25 years ago.

Scroll down to watch the first trailer for the movie. Oh, and don’t forget to mark your calendars for the release date of August 15.

If you haven’t read the book already, scroll down to shop the trilogy. We can pretty much guarantee it will be your favorite summer read: Crazy Rich Asians (Crazy Rich Asians Trilogy) ($9.60).

I’m Self-Employed: What Are My Retirement Options?

Good news: You have a lot of them. The challenge is figuring out which of the major retirement plans is best for you.

It used to be that only a few venturesome entrepreneurs would launch businesses on their own. The gig economy has changed that, with everyone from bloggers to Uber drivers to freelancers being seen as self-employed owners of their own independent businesses.

Being self-employed has its obvious perks, but it also means that you are responsible for protecting yourself financially. Unlike employees with access to 401(k) plans, it’s up to you if you want to set money aside for retirement and your golden years.

If you’re working as your own boss, there are plenty of retirement paths to explore. The most common retirement accounts for freelancers and those that are self-employed are SEP IRAs, Simple IRAs, and Individual 401(k)s. Similar to retirement accounts offered by employers, these retirement plans have two factors in common: up-front tax breaks and tax-deferred saving, meaning you don’t pay taxes until you withdraw the money years later in retirement (the Roth version of the individual 401(k) is slightly different.)

The various tax-sheltered plans vary in terms of when and how much you’ll be taxed, as well as the maximum annual contributions you can make. So, which one is right for you depends on how much you can save and whether or not you have employees. If you’re looking to set one up, your first step should be to consider how much you can afford to save without compromising your lifestyle – and how much you’ll need during retirement.

This can all get pretty confusing, especially when combined with owning a small business or being a freelancer. That’s why we’re breaking it down right here.

5 smart options you can consider to ensure you’ll have retirement savings available for your golden years.

What a Traditional IRA and How Does It Work?

The first option we’re going to review is a traditional IRA. With these, you contribute pre-tax earnings into your account and don’t have to worry about giving Uncle Sam a single penny until you withdraw that money down the line. Actually, Uncle Sam is the one giving you money here — at least temporarily. Since you aren’t covered by a retirement plan through work, your annual contributions to a traditional IRA may be completely tax deductible. This reduces your tax liability for the year, potentially leaving more money for you to invest toward your retirement.

So the potential drawback of a traditional IRA? You could end up paying more in taxes when you do eventually withdraw your money if you’ve moved into a higher income bracket or if the government has raised tax rates by that time.

Sign up for a Traditional IRA here.

What’s a Roth IRA and How Does It Work?

The second option is a Roth IRA. This type of retirement account treats taxes differently than a traditional IRA. With a Roth, you pay taxes on whatever you contribute from the start. So you don’t reduce your tax liability for the year, but you also don’t ever have to pay taxes on that money again. The good part? Whatever is in your account when you retire is all yours.

However, unlike traditional IRAs, Roth IRAs come with income requirement. If you fall within these income requirements, can afford to pay taxes on the outset, and/or anticipate that your tax rate will be higher down the line (because you expect to make more money), a Roth IRA could be a great option for you. But since we have no way of knowing what tax rates will look like in the future, having retirement accounts that treat taxes differently (e.g., both a traditional and Roth IRA) isn’t a bad thing.

With a Roth IRA, you can contribute a combined maximum of $5,500 per year — or $6,500 if you’re 50 years old or older — to all of your traditional and Roth IRAs. Now for your monthly rate calculations: $5,500 divided by 12 is $458.33. That’s how much you should factor into your monthly rate if you decide to go either the traditional or Roth IRA route. If you’re 50 or older, your retirement savings target is $542.

What’s the Difference Between a Roth IRA and a Traditional IRA?

In short, Traditional and Roth IRAs are both tax-advantaged accounts designed to help you save for retirement, but there are a few differences between them.

In a traditional IRA, all earnings grow tax-free, and contributions may be tax deductible depending on your financial situation. Withdrawals from the account in retirement are typically taxed as income, and withdrawals before 59½ are subject to a 10% penalty from the IRS.

In a Roth IRA, the earnings also grow tax-free, but contributions are not eligible for a tax deduction. Unlike a Traditional IRA, when you withdraw from a Roth IRA in retirement, the distributions are (usually) tax-free. Contributions to a Roth IRA can be withdrawn without penalty at any time. Roth IRA investment earnings can be withdrawn after five years for certain approved reasons, such as a first time home purchase.

In short, Traditional and Roth IRAs are both tax-advantaged accounts designed to help you save for retirement, but there are a few differences between them.

Note: Both traditional and Roth IRAs are subject to contribution limits.

What’s a SEP IRA and How Does It Work?

So you work for yourself — either full time or part time — and you’re totally killing it. Being the boss of you lets you work how you want, when you want, on the projects you want. You’re a master planner when it comes to the hustle. Now you’re ready to master-plan that retirement.

If that’s you, there’s a super-special type of IRA you should know about. It’s called a SEP IRA, and this is how it works.

Best features: Flexibility. There’s no need to fund the account until you file your return. So if your net income turns out to be higher than expected, you can make a larger contribution and trim your tax bill. If you have a bad year, you can reduce your contribution. Also, if you’re building a business on the side while still working for an employer who’s sponsoring 401(k) plan you contribute to; your contributions to a SEP don’t interfere with your current 401 (k) plan.

So the potential drawback of a SEP-IRA? : This plan may be costly eventually if you have employees, as opposed to contract workers because the money you put into a SEP counts as an “employer” contribution. You must make the same percentage contributions for all “covered,” workers, or those who are 21 and older who have been employed by you for at least three of the last five years and are expected to earn $550 in the current year. Your spouse is exempt. In most cases, you can deduct the contributions you make each year to each employee’s SEP-IRA. If you are self-employed, you can deduct the contributions you make each year to your own SEP-IRA.

A SIMPLE IRA

Also called a savings incentive match plan for employees. A SIMPLE IRA is designed specifically for small businesses and self-employed individuals. If you have a few employees, say, less than 10, who make more than $5,000, but far from six figures, and want to offer a plan for them as a perk, this is probably the retirement plan for you. It was designed for firms with no more than 100 employees.

A SIMPLE IRA is a little burdensome if you have a startup or are a fledgling firm. You’re generally required to make a contribution to match each employee’s salary reduction contributions on a dollar-for-dollar basis up to 3% of the employee’s salary or a flat 2% of pay – no matter what the employee contributes to the account.

Best features. Easy paperwork. It should take about 15 minutes or less to fill out the forms.

So the potential drawback of a SIMPLE IRA? You can’t contribute if you’ve already maxed out employee contributions to a 401(k) at your day job. Also, if you need to make a withdrawal from a SIMPLE IRA plan within two years of its inception, the 25% penalty is significantly higher than the 10% fee you’d be charged for early withdrawal from a SEP IRA.

Sign up for a SIMPLE IRA here.

✔️Solo 401(k)

A.K.A one-participant 401(k).or Individual 401(k), a solo 401(k) is similar to a traditional 401(k) offered by an employer to its employees. In other words, you can contribute to your plan as both the employer and employee.

Your contributions are pre-tax, so you’ll end up paying taxes when you withdraw your money later. As an employee, you can contribute a maximum of $18,500 annually ($24,500 if you’re 50 or older). As an employer, you can throw in 25% of your business’ earnings, though you’ll have to do some math to figure out your deduction limit.

The math here is the same as with the SEP-IRA. Experts recommend allocating $4,500 of your monthly rate toward retirement savings to max out your solo 401(k).

Sign up for Solo 401 (k) here.

You’re Getting Paid. Now Get Self Made.

Robo-advisors help streamlines the process. Unlike your typical human financial advisor, robo advisors are automated platforms that create tailored retirement and investment portfolios based on your financial goals and comfort level. They make it really easy to set up and manage your retirement and invest online. Ellevest, for instance, is a robo-advisor that seeks to “redefine investing for women.”

The company aims to serve women’s needs better than any other existing system by using an algorithm tailored specifically to women’s incomes and life cycles. (Believe it or not, no one else has thought to do this before).

Find out how to roll over a previous Roth IRA or traditional IRA here.

Automate Investing with a Robo-Advisor.

Think it involves too much management, set up automatic deposits for your retirement account(s). We get it. That’s why the best way to invest to automate it. An automatic transfer means you transfer a little cash into an investment account each month so you don’t easily spend it. Ellevest can get you set up in less than 10 minutes so you can reach all of your money goals. Sans judgment, finance jargon, and trust issues. Crisis, averted. Get into it here.*

Just started freelancing and your income is variable? Doesn’t that mean saving for retirement will be challenging?

Maybe, yes, but every little bit counts. So if you’re unsure about the dollar amount, perhaps shoot for a fixed percentage of each paycheck. It’s less stressful than trying to stretch a smaller paycheck, and you’re still getting into the habit of saving regularly for retirement. The experts recommend putting 20% of your income toward investing future goals (more on that breakdown here), including retirement; but if 10%, or even 5%, is what’s realistic right now, do that and work your way up as your rate rises.

And the sooner you start the better. That’s because of compounding, which Einstein is said to have called “the most powerful force in the universe” Your money starts working for you right away, and even small amounts can grow to large amounts over a long investing horizon. So, don’t let that fact that you’re a self-employed stand in your way—pick a retirement plan today and start saving.

You’ve got this.

Bottom Line

It can be fun spending money. It can be even more fun watching your savings grow. You’ll thank us later.

For when you don’t have a retirement fund…

Don’t sound the alarm – yet. Ellevest can get you set up in less than 10 minutes so you can reach all of your money goals. Sans judgment, finance jargon, and trust issues. Crisis, averted. Get into it here.*

Being an entrepreneur, small business owner, or freelancer is not easy…

The biggest challenge for many entrepreneurs comes is all managing you have to do. One way to make it easier on yourself is to automate with Honeybook, your all-in-one project, invoicing and payments management tool. HoneyBook’s robust features can help you manage everything and, yes, keep me on track with it all. Plus, Style Salute readers get 50% off their first year. Get it here.

Up next: In your 20s? For most of us, our 20s are a decade of #adulting, including with our money. So where do you start? Here’s a roundup of 4 steps to take now, from our friends.

Disclosures: We’re excited to be working with the team at Ellevest to start this conversation about women and money. We may receive compensation if you become an Ellevest client.

100 Chic Blouses to Dress Up Your Jeans

We will forever love tops that look good with jeans. A great top adds a special touch to any outfit and is always the best wardrobe staple. Shop here!

The Two Accessories You’ll Want to Wear With Every Outfit

Isn’t it the best when you find accessories that are so good, they match with every outfit? That’s exactly what’s happening here, thanks to Cult Gaia.

The brand’s ark earrings ($100) and mini bag ($320) have proven to be so wildly popular that they’ve out a whopping six times.

Keep scrolling to shop the ark earrings with a cult following, plus a few other styles we love.

The Personal Finance Tips Everyone In Their 20s Should Follow

Your 20s are an incredibly thrilling decade in your life. You’re advancing in your career, figuring out where you want to live, and making major decisions that will set the tone for the rest of your life.

And, while you’re 20-somethings are incredibly exciting, they can also be somewhat challenging.

For some of us, it’s the first time we are dealing with a lot of adult responsibilities like managing a paycheck, paying for rent, health care on our own, getting out of debt, and saving for our future. Adulting is tough, and it can all be very overwhelming – and that is exactly why it’s incredibly important to establish good personal finance habits now.

While investing in your 20’s may sound boring, starting young is easily the best way to get ahead.

“But, I can barely afford to make rent every month. Isn’t investing for when you’re older and making real money?” you might be thinking.

The simple answer to that is: No – you should absolutely be saving and investing for Future You. “By investing early, you can really build your wealth – and you don’t have to be an expert to do it,” says Sallie Krawcheck, CEO and co-founder Ellevest, the investing platform for women. All you need is answers to the right questions.

Thankfully, we tapped Krawcheck to lay out the five money rules that people in their 20s should always follow. Let’s get started.

✔️ Pay down your bad debt.

74% of women in their 20’s have debt, and 41% of you have high-interest rate debt.

What to do with credit card debt: First, work on paying your high-interest rate debt. Seriously, if you have any kind of balance on a credit card, stop using it and pay it off. Nothing is worse than paying 10-15% interest (or more). This interest is higher than any returns you could see from investing, so make this a priority and drop that credit card balance. Next, transfer any credit card balances you have to a 0% interest rate card. Then, use the savings to pay down more debt.

What to do with student loans: If you haven’t already, set them on auto-pay.

Doing this can typically reduce your interest rate by %0.25. You should also consider refinancing any interest rates that are in the double-digits. You’ve probably been hearing about refinancing from your friends, so why don’t you try it. It doesn’t hurt, and it could pay off a lot. You can use a platform like Lendkey to find, customize, and fund your loan through a network of credit unions and community banks. This way, you can see which lender can offer the best rates.

✔️ Build up your emergency fund.

37% of twentysomething women changed jobs, and 41% of you move in the past two years. You’re very busy!

What to do: Your first savings milestone is to build an emergency fund. This should be at least three months of take-home pay, in case you get fired (hey, it happens — more than any of us like to think), your roof caves through, or in case you have to take time away from work for, you know, an emergency. This emergency fund money should be held in cash, for safety.

Where to put your emergency fund money: While a lot of advisers charge for emergency fund or “safety” investments, we found that Ellevest charges no management fee for money held as part of an emergency fund.

This emergency fund is invested as cash in an FDIC-insured bank account and earns a trickle of interest, but it won’t lose principal either (like it would sitting in your bank savings). Also, seeing your emergency fun incorporated into your plan if you choose to keep it with Ellevest may help you get a more comprehensive view of your finances.

✔️ Get paid what you’re really worth.

28% of your twentysomethings got a promotion in the past two years. Congratulations! But, make sure you’re getting paid what you’re worth.

What to do: Starting with low pay can be a drag for years, since you get raises off that base. Slay the work, learn negotiation skills, practice in advance, and ask for the raises and promotions you deserve.

And the next step is…

✔️Invest in your future goals.

I know it’s far away, but if you’ve checked off all of the above – paid off your credit card debt, set aside your emergency fund money – it’s time start thinking about investing in your future goals.

Why? Because, as we mentioned, thanks to the power of compounding, a dollar invested in your 20’s is more valuable than a dollar invested in your 30’s or 40’s.

But, where and how should you get started? One of the best steps you can take is automating your investments so they can take care of themselves. The best – and easiest – way to automate investments is to sign up with a robo-advisor. If you’re unfamiliar with robo-advisors, they’re companies that provide automated, algorithm-driven financial planning services with little to no human supervision.

Ellevest, for example, is a robo-advisor dedicated to helping women invest by considering gender-specific financial differences – they also have no minimum to start investing so you can start investing with as little or as much as you like.

It’s also a lot easier to build real wealth when you’ve made saving and investing a priority instead of an afterthought.

Next up, asking for a raise? Here are 5 ways to figure out if you’re underpaid — and get even.

Disclosures: We’re excited to be partnering with Ellevest to start this conversation about women and money. We may receive compensation if you become anEllevest client.

The Best Way to Boost Your Income (Without Asking for a Raise)

For when you’re asking for a raise… Know your worth.

The job market is tight right now and depending on your job it can be a pain to hire and train someone new. This means employees often have more leverage than they think. Here are some tips:

You’ve heard it from us before, and you’ll hear it again: You should ask for a raise — because chances are if you do ask, you’ll get it (fact: 75% of women who negotiated for a raise got one in 2017). But, what if we told you that you could give yourself a raise even if you didn’t get the courage to ask for the raise — or you did and you struck out?

According to Sallie Krawcheck, co-founder, and CEO of Ellevest, an innovative digital investment platform for women, you could be making more money tomorrow (like a lot, LOT more) if you just start investing today.

The reason is pretty simple . . . by investing your money steadily today, you’ll be able to take full advantage of “the power of compounding”— the power of your investments to earn returns on the money you invest . . . and over time, you also earn returns on the returns themselves. And that will pay off.

And the earlier you start, the better. Why? Because a dollar invested in your 20’s is more valuable than a dollar invested in your 30’s or 40’s.

So that raise we were talking about earlier. . . yes, you should absolutely ask for it. But also invest the money you make already because it will make you more than even that raise.

Ahead, we go through why and how you should start investing today.

The Cost of Waiting is High

So how much are we talking about here?

It’s easy to think a raise will solve our “money problems,” but did you know waiting to invest can cost you big time? How high? About $100* a day for some of us.

To put it into more context, let’s say you’re earning $85,000 a year. Sadly, you didn’t get the courage to ask for the raise — or you did and you struck out. Hey, it happens. But you did decide to take your annual 20% savings and invest it in a diversified investment portfolio instead of leaving it in the bank (except for your emergency fund, of course).

How much more money will you have in 40 years? Ellevest estimates say anywhere from an additional $565,000 to $2.1 million more* (seriously, friends), depending on markets. So, on average, let’s call it $1.4 million more. That’s more than the incremental $1 million you get over time from getting that raise.

Starting is Easier Than You Think

At Ellevest, they’ve built a robust investing plan for you, based on what you tell us you want to achieve. And it’s flexible — so you don’t have to worry about doing it “perfectly.” You can sign up and drop a dollar in your account today and always change your goal timelines and monthly deposits as life changes. The important thing is to just start investing already.

Why We Should All Invest

We should invest because we are literally losing money if we are not. Fact is: We have less money than men, not because we don’t work as hard as men do (we know the answer to this one), and not because we’re not as good at math as men are (trivia fact; we’re as good or better at math) — and not because we’re not as good at our jobs or as good at investing (ahem–we’re actually better). It’s not for any of these reasons.

Simply put, women don’t invest as much as men do. And they don’t invest as early as men do.

So, why are we not investing? It’s because the financial services industry has been built by men, for men. . . until now.

Enter Ellevest. The new way to invest: Built for women, by women — with hundreds of hours of research, design, and conversations with women about what they actually want. Brought to you by a company populated by people more representative of what our country actually looks like (since we’re not 90% men).

Built with women in mind, Ellevest’s unique algorithm takes into account the realities of being a woman. Realities like: we live longer than men, our salaries peak sooner, and we take career breaks, i.e., we have kids. Pretty important stuff when it comes to retirement.

Whatever your reason, it’s time to start investing towards your goals. You don’t need to know everything. . . you just need the basics we’re giving you here. And believe us, starting is the hardest part, but we’re challenging you to take that first step today by taking away all your excuses for not.

Where Do I Start Investing?

Why Ellevest?

There’s investing, then there’s Ellevesting. Ellevest has built into their proprietary algorithm women’s unique salary curves and longer lifespans, to give you an investment plan designed to help you achieve your goals in the majority of market scenarios.

The platform is well-designed, easy-to-use, and speaks to our unique financial needs — whether that be planning for retirement, that Aussie vacation, or starting a family. The best part? The advisors at Ellevest are incredibly knowledgeable and will help you every step of the way.

What are you waiting for?

If you had a dollars falling out of your purse every day, you’d get that fixed, right? This is the same thing — let’s fix it today. Repeat after us: “Yes, I will absolutely ask for the frickin’ raise. But I will also invest the money I make already.”

Now that you’ve read about how to boost your income with investing, it’s time for you to develop a game plan for your money.

Adding These 10 Products to Your Summer Beauty Routine Will Change Everything

Summer heat is a welcome change from blustery winters, but can create its own issues with beauty. Whether you’re going for a summery wardrobe, or boldly trying out a new hair color, it’s crucial to test out some new beauty routines and adapt to the season’s sun-soaked activities.

Below you’ll find 10 of the beauty products that we swear by as part of our summer beauty routines.

Mary Kay TimeWise Anti-Aging Tone-Correcting Serum

This lightweight serum not only reduces the visibility of sun damage and dark spots on the face, it also brightens your skin’s overall tone. Two quick daily applications allow the serum ample time to soak into your skin and repair any damage you may have gotten during your long summer days in the sun.

Complexion Rescue™ Tinted Hydrating Gel Cream from bareMinerals

We all know how damaging UV rays can be after hours spent out in the sun, but how many of us actually remember to put on sunscreen in the morning? Combine many different needs with this lightweight tinted moisturizer containing SPF. The hydrating cream nourishes your skin while protecting it from sun damage to give you a bronzed look.

Schick® Hydro Silk Women’s TrimStyle® Razor

Investing in a good razor is an essential summer beauty choice. Beach days and short shorts don’t need to be ruined by unsightly bikini lines or scratchy legs. Schick’s Hydro Silk Razor offers five Curve Sensing® blades to fit all your curves without irritation to make sure you get the best shave possible. It can also be flipped into a trimmer to maintain your bikini line in and out of the shower!

OUAI Leave In Conditioner

Frizzy hair is one of those inevitable evils that accompany summer heat. Beat it by spritzing some Ouai Leave In Conditioner into your hands and running them through your locks. It’s paraben-free and has no drying alcohols that dehydrate hair so it leaves hair shiny and smooth.

Not Your Mother’s® Beach Babe® Texturizing Dry Shampoo

If you can’t get to the coast, you can still get beachy waves with Beach Babe. This spray’s cruelty and paraben-free magic will reduce unwanted oil and grease in your hair and leave it smelling fresh. It will also help boost your hair’s volume and get you ready for any adventure.

ORIGINS Clear Improvement® Active Charcoal Mask to Clear Pores

This ultra-purifying face mask helps many different skin types, including oily, dry, and sensitive. It works to deep clean your skin and shrink your pores. The charcoal in the mask removes oil while the clay absorbs toxins that might have built up in your pores. Use it twice a week to see visibly clearer skin and smaller pores.

NYX Makeup Setting Spray- Matte

Getting a makeup setting spray that will outlast sweat and pool water is essential if you’re going to maintain a beauty routine throughout the warmer months. This matte spray from NYX Cosmetics is lightweight and doesn’t leave a shine behind to give you all-day protection for every adventure the summer brings!

COOLA Organic SPF 30 Scalp & Hair Spray

COOLA Organic Sunscreen Body Spray | SPF 30 | Certified Organic Ingredients | Farm to Face | Ultra Sheer | Eco-Lux Size | Continuous Spray | Water Resistant | Unscented

COOLA Organic Sunscreen Body Spray | SPF 30 | Certified Organic Ingredients | Farm to Face | Ultra Sheer | Eco-Lux Size | Continuous Spray | Water Resistant | Unscented

36

SHOP

It’s not just your skin that needs protection from the sun, but your hair and scalp as well! Try out this scalp and hair mist to shield your locks from color-stripping and drying UV rays, and keep your scalp from getting sunburned. The product’s Monoi Oil nourishes your hair while the other organic, antioxidant-rich ingredients show your hair some natural love.

Make Up Forever Artist Rouge Lipstick

This lipstick is luminous and lightweight and contains Vitamins C and E to nourish your lips as you go about your day. It also comes in several bright colors to experiment and customize your own look. The Rose Wood color is a good color to experiment with because it’s bright and poppy but not too gaudy. It will help brighten your face and match that new sundress that you’ve been waiting to bust out.

Le Volume De CHANEL Mascara

There’s nothing worse than emerging out of a pool with raccoon eyes. This water-proof mascara gives high-precision lines and volumizing color that won’t smudge in water. Chanel’s exclusive brush will make your eyes pop and the long-lasting color will draw attention to your face.

Next up, the products makeup artists recommend for hot summer days.

The Beauty Service We’re Obsessing Over + A Giveaway!

As beauty editors, our dreams tend to differ from most “normal” people—they usually almost all involve lipstick, cream blush, and facemasks, for example. But one fantasy we think we do share with the common public is getting a beauty pampering treatment at home.

And since we know all of you reading are beauty lovers too, we partnered up with beGlammed, the leading on-demand beauty service that delivers professional hairstylists, makeup artists and nail techs straight to your door, to gift 1 lucky winner a $150 gift card good toward beGlammed services. Head to our Instagram page to enter the giveaway. Details below.

The prize:

- A $150 gift card good toward @beGlammednow hair and makeup services.

- To enter:1. “Like” – Head over to Syles Salute and beGlammed Instagram profiles and give us a like!

2. Comment – Like the photo and tag 2 beauty loving friends who would LOVE to win this gift card

3. Wait – We’ll announce the winner a week from now, on August 3rd, 2018.The Fine Print-This contest is open to residents of the U.S. only.

-Winner will be contacted via their Facebook account. If our team does not hear back from you within 24 hours, a new winner will be selected.

-Limit one comment per entry. Multiple comment entries will not be considered

-This giveaway ends at midnight on Tuesday, August 3rd

-This is not a sponsored giveawayGood luck!

The services you could win!

Blowout or Dry Styling

From damp to dry, sleek and chic or full and voluminous, beGlammed’s bombshell blowouts are a favorite. If your hair is dry when your stylist arrives, dry styling includes curls, waves, flat iron or braids.

1 hour, starting at $50

Blowout + Styling

A gorgeous bombshell blowout with your choice of dry style.

1 hour, starting at $70

Updo

Any updo from a beautiful bun, chic chignon, pinup pompadour or elegant twist. Half-up, half-down hairstyles are considered updos.

1 hour, starting at $85

Makeup Services

Makeup

Full makeup application (faux lashes not included)

1 hour, starting at $75

Makeup with Lashes

Full makeup application including faux lashes.

1 hour, starting at $95

Airbrush Makeup

Full makeup including airbrush application (faux lashes not included)

1 hour, starting at $105

Airbrush Makeup with Lashes

Full makeup including airbrush application and faux lashes.

1 hour, starting at $125

Makeup Touchup (only available when booked with another service)

Put the finishing touches on your look.

15 minutes, starting at $30

Group Makeup Touchup (for groups of 3 or more)

Put the finishing touches on your look.

15 minutes per person, starting at $25 per person