For when you’re asking for a raise… Know your worth.

The job market is tight right now and depending on your job it can be a pain to hire and train someone new. This means employees often have more leverage than they think. Here are some tips:

PHOTO: @collagevintage

When I walk toward’s my bosses office to ask for that raise, I start to feel the same combination of fear and embarrassment, usually reserved for when you show up at a party underdressed. In an effort to gain the courage to one-day actually make the ask, I decided to take a step back and learn a few simple and achievable negotiation tips that will work.

To paint you a picture, I’m 28 years old with a mid-level job, student loans, and a not-so-cheap loft in Los Angeles. Although I’m working hard and I know I’m doing well, I haven’t gotten a raise in over 8 months.

Fortunately, in my furry of internet searches, I found an excerpt from the S.H.E. Summit in New York City in October that helped a lot. At the summit, Sallie Krawcheck — the former Wall Street executive and founder of Ellevest, a digital investment adviser for women — spoke about how women can proactively bridge the gender pay gap. Her advice in a nutshell: Don’t just ask for a raise — provide definitive proof that you deserve it.

Here’s exactly how she recommends doing it.

Step 1: Evaluate How Much You’re Worth

Before you do anything about anything — do not pass go, do not collect $200 — figure out how much you’re worth. There are some great resources to help you do this that can take less time than your morning commute.

Start with Comparably, which provides average salary data specific to your industry, function, and geography in under a minute. Hired.com will show you up-front job offers from potential employers including compensation numbers after you’ve answered a few questions. GetRaised takes you one step further, not just with calculations of your pay gap, but with step-by-step instructions on how to approach your boss to get the best results. It doesn’t matter what you use, one or all three — the first step to getting paid more is identifying a gap between your current salary and your market value.

Step 2: Identify What Success Looks Like for You

Once you know what you’re worth and what your bank account’s missing out on, it’s time to take action and get that raise. This is how you can get what you want in a negotiation.

Monday morning, schedule a one-on-one to have the “what does success look like for me?” conversation with your boss. This should happen now, not six months from now or during your next performance review. That’s because it should take place far enough in advance of your performance review so that you can do something about it.

If at all possible, ask for specific numbers, so that when it comes to review time there’s no room for disagreement. Examples of key performance metrics include how many new clients, completing which project by what deadline, how many hires, what type of customer satisfaction rating, what revenue target, how much in expense cuts, or what type of efficiency improvement. You get the idea.

You should also gain a clear understanding of how (s)he wants to see you develop as a professional, whether it means taking on a greater leadership position, gaining more marketing experience, or starting a new project.

Step 3: Focus on the Mutual Win

Have the “what does success look like, not just for me, but for our business?” conversation with your boss. This will position you psychologically on the same side of the table as your new manager. Your salary isn’t something that will deplete the company; it’s something that helps the company flourish! In fact, the reason you’re being hired is to generate value for them. By understanding what success looks like for your department or your business, you can potentially aim your career that way. For example, if it’s all about growing the product that was brought out a few months ago, you can gear your efforts toward that.

Don’t just negotiate for a salary bump. You can also negotiate benefits, equity, flexibility — and anything else that matters to you — as a bundle. Negotiating piece by piece can accidentally make both of you feel like you lost. Understanding which items matter more to your boss, which items matter more to you, and where they’re the best deal is for both of you is entirely possible with good communication.

Here are some ideas for “non-money” perks you can ask for:

Questions? We’re here to help. Leave us a comment and we’ll get back to you!

Disclosures: We’re excited to be teaming up with the team at Ellevest to start this conversation about women and money. We may receive compensation if you become an Ellevest client.

When you’re in your twenties, it can be hard to look far into the future when you’re not completely sure what the next couple of years will hold for you – and sadly, there’s no ‘Magic 8 Ball’ here to tell you what’s in store for your future (sorry ladies.) But, amongst all of those concerning life questions that have the tendency to pop into your mind as a young adult – “Where will I be living?” “Where is my career going?” “What do I want to do with my life?”, it is vital to invest in your personal happiness. Yes, those life-related questions are important when evaluating your life success, but investing in, or experiencing moments that make us truly happy is definitely a top priority.

It’s no secret that everyone is the best version of themselves when they feel their absolute best. It can be devoting your time to something small, like purchasing that lipstick that’s the perfect shade of red or drinking an exceptionally good cup of coffee every morning. It can possibly be something more extravagant, like finally taking that Mediterranean cruise you’ve been dreaming about or signing a lease to your first apartment. Just remember, whatever helps you feel like your best self is an investment worth making.

Keep reading for the investment-worthy pieces that you’ll want to save up for below.

1. A go-to professional outfit

As a woman in your twenties, and whether you’re into fashion or not, having a go-to professional outfit is key to being prepared for important life events that come your way. Whether you have a job interview, fancy dinner, wedding or networking event, giving off an exceptional first-impression can showcase your ability to get a job offer, act sophisticated in a professional environment and define your personality through your sense of style.

Find the perfect “power suit” is about finding what pieces enhance your shape and define your style. Ultimately, you have to feel confident in what you wear, especially to a special event. Here are some clothing items to look for in shaping your go-to professional outfit.

Blazer: this can go with just about everything. You can dress it up or down with dress pants, jeans or skirt. Most likely, a black colored blazer will coordinate with most outfits, but if black isn’t your color of choice, try another neutral color or a bright colored blazer as a statement piece in your closet. Here are a few editor-approved blazers you’re going to love.

Black dress: A true classic! A plain black dress can be worn by itself or paired with really fun accessories and shoes! It’s essential to have in your closet because you can wear it to almost anything. Not only is it perfect for work but it’s great for a casual outing as well, making it easy for you to hit up happy hour with no need to stop at home and change! Need a new black dress (Always). Check out these black dresses from Revolve that are perfect for those desk-to-dinner days.

Black heels/or slip on: No woman in the world should go without a classic black heel. When you’re looking for a pair of shoes to complete an outfit, you’ll be glad you invested in these; as they will be your go-to option for completing an outfit. Heels can have the potential to be uncomfortable, so if you don’t want to take that risk, try to opt for a shoe that is generally more comfortable. Fashion labels, Sam Edelman and Steve Madden are always a great go-to if you’re in the need of any work appropriate sandals, mules or flats. Personally, I love the Ariella heel from Sam Edelman. It’s only $100 and looks like a million bucks. Here are a few more black heels that are equally great.

It is highly encouraged to take care of your skin while it’s youthful to prevent or reduce the skins’ common signs of aging. Products like a face wash, toner, moisturizer, and sunscreen help to clean, brighten and clarify the skin’s surface. Their quality ingredients or additives have the power to benefit your particular skin type as well! If you have particularly dry skin, look for aloe vera, ceramide or hydraulic acid on the ingredients label. For an oilier complexion, try products with tea tree, glycolic acid, or a clay mask to eliminate shininess. Depending on the condition of your skin, you may want to see a skin care professional for an additional opinion. That way, if there are certain products or ingredients that need avoiding, you’ll know before purchasing anything that can be harmful.

In addition to facial products, using lotion or a body oil to moisturize your body can keep it give it healthy and hydrated. The best time to use a lotion is right when you get out of the shower. That way, the product can help thirsty skin pores from the hot water. Remember, finding the products that work the best for skin type won’t happen immediately. But, once you find something that works, make a consistent routine a must!

Looking for investment skincare on a budget, you’d be surprised how much amazing skincare you can find on Amazon. Here

It’s hard to feel like a fully functioning put-together adult if you find your undergarment drawer filled with holes in your underwear and wires poking out of your bras. If you want to be a badass #girlboss, you have to have the intimates to match. With a study that showed that the average woman will spend over $4,000 dollars on bras in her lifetime, it only makes sense to make the investment now and buy a bra that will actually last a lifetime! In today’s world of comfort being key, women are now able to buy bras where comfort is the main priority.

Bra companies like True & Co. have made it their mission to create the perfect bras for women that are as comfortable as possible. By collecting data from over 6 million women, adulting has never looked so easy. No matter what life situations are thrown at you, it’s worth it to know that you’re wearing a bra that can support you through all of it.

Planners are fantastic organizational tools that should be used on a daily basis. Whether it is for work, fitness goals, budgeting, or just daily life in general, planners basically make you an organized queen. They can assist you in making more intentional choices, allow you to be creative and make it easier to remember important deadlines or appointments.

Trying to remember things from memory is not worth the stress when you can easily write things down. With planners becoming extra colorful, customizable with stickers and post-its, and more in-depth with calendar categories, you can remember your to-do’s in a fun and stylish way!

There’s nothing like coming home from a long day and watching your favorite Netflix show on your silky comfy sheets. Making the splurge and buying a set of quality sheets really makes all the difference, not only for your time of relaxation but also for your overall sleep. Guru site on all things sleep, The Sleep Sherpa, recommended buying organic linen sheets for your best possible version of a night’s rest. The article states that not only is purchasing organic better for those with skin conditions such as eczema but linen has been shown to help regulate your body temperature. Buying organic linen will be sure to rid your worries of any possible tossing and turning.

No matter how big or small the item or experience may seem, what you’re essentially investing in is your happiness and the best version of you. No one can ever put a price tag on that! What are some of your recommendations for twenty-somethings to invest in?

For us gals, every day is the big day. And we want nothing more than to rise and shine, look in the mirror, and see a well-slept, glowing complexion staring back at us. So, we stick to the beauty tip we know best. We get our “beauty sleep”.

But let me guess — no matter how many hours of zzz’s you manage to squeeze into one night, you know you could be getting more restful sleep. Truth is, women that have great skin aren’t necessarily getting any more sleep than you, they simply have bedtime rituals that put them in a rested mindset — and as a result, they have better sleep. Which you guessed it — helps improve the radiance of their skin.

So, what does it mean to have a bedtime ritual? Instead of jumping straight into bed, these women take a few minutes just for winding down and pampering their skin. To help you get your best beauty sleep ever, we’ve put together the top ten bedtime habits women with great skin swear by.

Ready. Set. Let’s glow! Scroll through for 10 bedtime habits that all women with great skin do.

If you’re looking to get better skin overnight, a silk pillowcasewill do the trick every time. Our nighttime routines involve a range of products and rituals, but this is possibly the most important. Silk pillowcase help protects and hydrate the skin, reduce split ends and keeps frizz at bay. Scroll through to shop the pillowcases that will promise to give you better skin by morning.

If you want to wake up with a fresh face, removing all of your makeup is a must. No matter how much makeup you’re wearing, or how exhausted you may be, the extra five minutes to remove your makeup can work wonders. Leaving on makeup clogs your pores, and prevents your skin from renewing when you sleep. With a jar of cotton balls and one of these makeup removers on your bathroom countertop, you won’t forget this ritual.

Also, after washing your face, apply a facial toner that makes your skin happy. Using a toner is just another way to rid your skin of any extra oil, dirt, or makeup. With a few drops of these facial toners on a cotton pad, you can say goodbye to breakouts and acne.

Nothing beats the touch of a baby’s skin. But if you exfoliate after removing your makeup, you won’t be able to keep your hands off your skin. A small dab of exfoliating creme and a gentle rub will leave your skin feeling refreshed and smooth. Exfoliating removes the natural oils, dirt, and any dead skin cells that collected during the day. With these exfoliating creams you will wake up flawless.

Did someone say spa night? For hydrated skin apply a face mask. Not only is it fun to pretend you are at the spa, but it helps to remove excess oils and purify your face. Also, when a face mask drys and tightens the skin, it helps with blood circulation, resulting in a bright and smooth skin tone when you wake. Pamper yourself with these face masks—and don’t forget to add the cucumbers.

Want to make sure you get good zzzs wherever you are? A Casper mattress is the answer. It’s super comfy and all about the memory foam. Plus, they offer a love it or we’ll take it back guarantee. Say hello to your new fave way to sleep. Nearly 4 million people love this mattress and “don’t remember how they slept before it.”

These extra-long staple supima cotton sheets ar four times stronger than the industry average and one of the finest and longest fibers in the world. It won’t pill or wear thin — it will only get softer with every wash

Who doesn’t love a bedtime story? Always keep an intriguing book on your nightstand. Reading a chapter or even a few pages will distract you from any thoughts that might be keeping yours from sweet dreams. This will help to reduce the production of cortisol, which can lead to skin outbreaks. Plus, reading is exhausting, so your eyes will quickly shut. Anyway to fall asleep quicker will give your skin some extra rest and minimize dark circles.

It may seem uncomfortable at first, but pinning your hair backis one of the easiest ways to keep your skin healthy. The oil and dirt from your hair collect on your face and pillow, which increases the likelihood of breakouts. You can easily avoid this by using one of hair accessories to keep your locks away from your face.

Running a humidifieron a warm mist while you sleep will keep your skin hydrated and soothed. The humidity hydrates your pores and helps to eliminate dry, cracked, or itchy skin. Say goodbye to chapped skin with these humidifiers.

Flowing through a few yoga downward dogs or taking a moment for meditation will help you to wind down from a long day. Yoga increases blood circulation to the head and face, stretches and strengthens your skin, and reduces stress. Using the below yoga props you can find ways to bring oxygen to your skin, reduce acne and pimples, and brighten your complexion.

Stay youthful by keeping the sensitive skin around your eyes moisturized throughout the night with eye cream. All you need is a small dab below the eyes, and the magic will happen over night. The ingredients in these eye creams will help to reduce wrinkles, blemishes, dry skin, and puffiness.

As every Kate Middleton fan knows, she loves mixing high and low pieces (and also re-wearing them)—which is one of the many reasons why we love her. During the Duchess visit to the London Marathon, she was spotted in a perfectly polished approach to athleisure, wearing an all-black ensemble and her favorite pair of sneakers.

We first spotted the Duchess wearing the affordable Superga’s Cotu Classic Sneakers ($65) back in October where she paired the shoes with a striped Luisa Spagnoli Pullover ($280) and simple blue skinny jeans. Now, she brings them out again for a Heads Together event ahead of the London Marathon. The versatile sneakers are also loved by Karlie Kloss and Gigi Hadid.

If you don’t own the classic sneakers yet, it’s high time you do: They have 600 reviews on Amazon right now, and they ring in at a reasonable $65. They’re under $100, and they’re Kate-approved—need we say more?

Keep scrolling to see the different times Kate Middleton wears the sneakers, and shop her shoes below.

Why is investing important? It’s a good question. If you’re already managing a budget and paying down debt, you might wonder why you have to add another financial task to your already long to-do list. But the truth is, money is power. And this one “to-do” might be the most important of all.

The society we live in is a capitalist one, and money steers it. It plays out in business; it plays out in politics and the way our country is run (or not), and it can even play out in our personal relationships. So, investing your money is an important way of helping you accomplish your specific, real-life financial goals. This includes goals you might already be saving for but may not have ever considered investing toward, such as buying a home or starting a family.

Here’s the math: (Women making less than men) x (Fewer women investing) = Women having way less money than men.

We’ve said it before, and we’ll keep saying it — we really, really need to fix the gender investing gap. It’s 2018, and we have come a long way. Arguably, this may even be the most powerful generation of women ever.

We women are more educated, accomplished and empowered than ever before. But when it comes to women investing and managing our money, it feels like we’re stuck in the 1950s. In fact, according to a new report from UBS, 56% of married women leave investment and long-term financial planning decisions to their husbands, and 85% of women who defer to their husbands believe their spouses know more about financial matters.

At a time when women control nearly $40 trillion, why is the situation getting worse, not better?*

As women, we need to pave the way for our ourselves and generations of women to come, and finding financial security is key to accomplishing this independence. But, as someone who doesn’t “speak finance,” how can you protect you money and have it work for you? The good news: investing is not that scary, and you don’t have to know a whole lot about the stock market to make good investments. Sallie Krawcheck, co-founder and CEO of Ellevest, says that by following a few basic investing tips, you can even get started today — even if you’re on a budget.

Here are eight simple, actionable tips she recommends to protect your money and make it grow.

1. Educate yourself

Keeping your hard-earned cash under the mattress (or, you know, in a savings account) can cost you, big-time. Sure, saving money in the bank feels like a safe thing to do. That’s because you don’t ever see your account balance go down (unless you withdraw it yourself).

But there is a risk: If you’re only saving your money, you may be unable to reach your financial goals. Many of us need to grow the money we save in order to reach our goals —which is what investing is all about.

Putting your money in a savings account may sound the right thing to do intuitively, but it ignores the power of compounding. Here’s an example of compounding:

Say you invest $25,000 in a savings account, after 35 years of earning interest, you’ll end up with $35,391 or more, assuming a range of many different economic scenarios.* And you’re guaranteed not to lose that money. However, if you instead invest that $25,000 in a well-diversified portfolio consisting of 60% stocks and 40% bonds, your account will grow to $54,348 or more in 35 years, under the same economic scenarios.*

Bottom line here: If you want to retire, you have to invest. Whether it is through your 401(k), IRA, or your own personal investment portfolio, you need money to work for you (only you working for it).

See how an investment plan could help you manage your finances. Ellevest is one way to do it. You can get a personalized portfolio in under 10 min. And it’s made by women, for women. Follow the link below and you’ll be taken to Ellevest for more information.

2) Take advantage of retirement accounts through your employer

Did someone say “free money?” Yep … it was your employer. If you have a 401(k) employer match available to you, it’s in your best interest to take full advantage of that. (aka max it out.) Here’s how a 401k match works and why that’s the case.

The first step to investing is to understand your work-sponsored retirement plans. This step is crucial and quite simple. Your employer likely offers a 401K and may even match your contributions up to a certain percent. This is the first step to investing for retirement, but not the only one.

Self-employed? Good news: You still have options for retirement plans. The challenge is figuring out which of the major retirement plans is best for you. If you’re your own boss, see what your retirement options are here.

Left a job recently and don’t know what happened to your old 410(k) plan? Not to fret: that money is still yours. It may be with your old employer, or maybe it’s in an IRA. But, wherever it is, if your money was invested, it should still be growing. So, you’re going to want to find it and put to use. Here’s more on how to do with your old 401(k)s. If you don’t have a retirement fund already in place (for example, a 401(k) or an IRA), start one immediately or you can roll over your old 401(k)’s to an IRA with Ellevest.

When you start investing, there are a few different approaches you can take. You can choose to manage the money yourself, or you can turn to a full-service brokerage and have an investment advisor manage your money, or you can use a robo-advisor.

Because of the high fees associated with managed investments, handing off investment decisions to an advisor isn’t the right approach for many people. Instead, you’ll likely choose between managing investments on your own or investing with a robo-advisor, which means an algorithm picks diversified investments for you based on your risk profile and investment goals.

Ellevest is a robo-advisor that seeks to “redefine investing for women.” This digital investment platform was founded by former Citigroup and BofA C-Suite executive Sallie Krawcheck whose mission is to help women to reach their financial and professional goals. They’re committed to helping investors reach their goals, and they provide tools to understand financial tradeoffs.

To get started, you would build a profile in five short steps. Based on your profile, Ellevest will suggest personalized investment portfolios for each of your goals. They are also fiduciary, meaning they act in your best interest (some investment advisors don’t act in their clients’ best interests). So, if you want a totally hands-off approach without paying a fortune for investment advice, robo-advising may be the way to go.

Now that you’re starting to think about saving for retirement, consider your other financial goals. Make a list of what you want for your life in the next 5 years and in the next 20 years. If you are hoping to start your own business, for example, this is something you can start planning and saving for. Your financial goals go well beyond retirement. If you want to travel the world one day, you must determine how much you will need to comfortably do so.

5. Continue your education in the workplace

No matter what industry you are in, chances are you have the desire to learn and grow. After all, gaining a higher level of responsibility, knowledge, and income is a goal that most people share. Continually developing yourself professionally will help your career and financial future in the long run, leaving you comfortably retired as well as proud of your hard-working, bada$$ self.

6. Invest in companies with female leadership

As they say, in order for our world to change, we need to be the change. Investing in companies that have values aligning with yours is actually easier than you may think. Financial firms such as Ellevest offers Impact Portfolios, which strive to earn a competitive return on your investment while creating positive social and economic change, ultimately benefitting women.

7. Look for an advisor you feel comfortable with

This is a biggie. Do your research and find an advisor you feel comfortable with. You choose a family doctor that listens to your concerns, so why wouldn’t you choose someone to handle your family’s financial health with the same regard? If you want a totally hands-off approach without paying a fortune for investment advice, roboadvising may be the way to go. As we mentioned above, “former First Lady of Wall Street” Sallie Krawcheck launched the female-focused investment platform that provides jargon-free services tailored specifically to women’s financial patterns (for instance, our salaries tend to peak earlier, we live longer, and we’re more likely to take career breaks).

Rather than shower you with questions about risk tolerance, Ellevest has you fill out a thorough online survey, and then tailors your investment strategy accordingly.

8. Make investing a habit

At Style Salute, we are obsessed with the power of habit. We know that adopting a new practice and doing it consistently is really hard, but it really pays off. And investing is no different. If you’re not sure how much to invest, Krawcheck recommends this ratio: 50% for needs/30% for wants/20% for investing, but it’s not a one size fits all thing.

Do what works for you, just invest some percent of every paycheck, and get yourself in that habit of investing, whether it’s with every paycheck, every week, month, or quarter. Make it a routine like brushing your teeth.

Need help? Ellevest’s team can guide you through every step of putting your financial plan together, and it only takes a few minutes.

Leaving a job means dealing with plenty of change, including saying bye to coworkers, packing up work life, oh yeah, and some more practical things you have to deal with, like what to do with your old 410(k) plan.

The good news: that money is still yours. It may be with your old employer, or maybe it’s in an IRA. But, wherever it is, if your money was invested, it should still be growing.

The other news is that leaving your old 401(k)s or IRAs behind typically is not a great idea. You’re going to forget about them. You’re not going to be watching them. The asset allocation will be off, and it’s going to potentially hurt you.

Ideally, you want to consolidate them in one place. But how? That’s where we can help.

Here’s what you need to know about the life-changing magic of tidying up your retirement plans.

When you move the money into an IRA rollover account, your money continues to grow tax-deferred, but you are no longer limited to the investment choices within your old plan. Make sure you choose “direct rollover” as the method for moving the money from your old employer into your new rollover IRA so you don’t get hit with taxes.

2. Move the Money Into your new Employer’s Plan.

This is an option, but you have to check with your new company: Not all defined contribution plans allow this move.

3 Leave the Money Right Where It Is.

You do have the option of leaving your funds in your old 401(k) plan, but there are a few downsides to doing that. One, you can no longer contribute to it; and two, you’ll have multiple 401(k) plans floating around you need to keep track of and that’s just confusing.

4. Cash Out and Take the Money as a Distribution.

This is not the best idea, because your money will no longer have the advantages of tax-deferred growth. Worse, you’ll pay income tax on the entire amount of the distribution, and you’ll be hit with a 10% early withdrawal penalty if you aren’t yet 59 ½ years old. In other words, don’t do it.

We like to cover all our bases here at Style Salute so here are a few other 401(k) related questions we get asked pretty often.

I’m New to Retirement Planning. Where Do I start?

If you’re new to the whole retirement thing, you can start fresh with Ellevest. Their friendly and knowledgeable concierge team can help you decide if it makes sense to move your money into an account at Ellevest. Or, if you have an existing IRA, you can transfer it over to an Ellevest account so you can pursue your unique retirement goals.

I’m Self-Employed: What Are My Retirement Options?

So you work for yourself — either full time or part time — and you’re totally killing it. Being the boss of you lets you work how you want, when you want, on the projects you want. You’re a master planner when it comes to the hustle. Now you’re ready to master-plan that retirement.

You can choose from a Roth IRA, Traditional IRA (you don’t pay taxes on these funds until you withdraw the money), or a SEP-IRA. Each of these retirement plans has its own rules when it comes to contribution and withdrawal, so do your research before deciding on the best one for you.

What’s a SEP IRA and How Does It Work?

If that’s you, there’s a super-special type of IRA you should know about. It’s called a SEP IRA, and this is how it works.

I Have Lots of IRAs and old 401(k)s at different places. What Should I Do with Them?

STEP 3: If you decide to move your account to Ellevest, you’ll call your provider and initiate the rollover (Ellevest can help with that call too).

STEP 4: Finally, when your rollover is complete, you’ll see your retirement accounts on one clear dashboard. Get started today.

Aside from a 401k, it’s important to consider other investment plans for your future. Only 46% of working women have retirement plans, and they’re falling short when it comes to investing as well. It’s time we close that gender investing gap and start taking control of our money. After all, as Ellevest CEO Sallie Krawcheck, whom I mentioned earlier says, “money is power.” Investing is your shot at growing your wealth, so why not take it?

Disclosures: We’re excited to be teaming up with the team at Ellevest to start this conversation about women and money. We may receive compensation if you become an Ellevest client.

Don’t get us wrong—we love our heels and wedges, but sometimes there’s nothing better than slipping on a pair of comfortable flats. The best part? With an option for every personal style, it’s hard to pick just one.

Travel during the holiday weekend is often cited as the most stressful time of the year. Between the longer than normal TSA lines to beating jet lag, getting to your destination can be seriously stressful—but it doesn’t have to be.

Have you ever noticed how frequent fliers never seem to sweat the small stuff? This is because after logging many hours in the air these fliers know that a well-curated bag can make all the difference.

While it might seem trivial what to pack, it’s not, and it can make all the difference when it comes to helping you fall asleep mid-air, protect your health, and help you actually make your flight an enjoyable part of the trip.

Curious to know what items frequent fliers swear by, we turned to seasoned travelers and mined Amazon to find the genus products that belong in your travel bag. From sleep balm that will put you right to sleep to smart luggage that lets you charge all your electronic items, these items help jet-setters arrive at their destinations fresh and ready for quality time.

Keep reading for the must-have items to pack for a stress-free holiday trip.

Thanks to the popularity of fanny packs these days, this safe travel item is one of the hottest accessories on Amazon. A money belts lightweight design helps to keep a low profile from prying eyes. It can be positioned between layers of clothing, hidden under clothes or inside your pants. Keep your valuables away from the sight and reach of thieves. Here are our favorites.

I know I’m not alone when I say that one of the biggest headaches during travel is finding a place to charge your phone and other devices. Especially during the holidays when you’re juggling so many different parties and events, your phone will be running out of juice a lot sooner. Smart luggage is the answer to this woe. These suitcases come with a built-in battery and are lightweight for easy travel. Genius? We think so.

If you’re traveling with liquids like perfumes, serums, or hair products, you know all too well the worrisome feeling of if they will spill all over your bag. This genius waterproof beauty bag from Tancendes will ensure your clothes and belongings will stay nice and dry in the event of an accident.

One sure way to de-stress while travelling? Listening to relaxing meditation music using noise-cancelling headphones. Ear plugs are now a thing of the past. These are essential for blocking out the plane engine, screaming baby, and snoring seat mate. These beauties have over 500 reviews and 5 stars on Amazon.

Having a dead phone battery while traveling is stressful and unnecessary. Airports often have minimal outlet space and nothing is worse than sitting on a laminate floor waiting to get your phone past 20% battery. Portable chargers are a life-saver. The Anker PowerCore 10000 is sleek and light, plus it has 4.5 stars and nearly 7,000 reviews.

Eye masks are essential for catching shut-eye while traveling. This soft plush mask has built-in Bluetooth headphones. Perfect for blocking out light and sound.

Facial skin becomes dry and eyes become puffy while 30,000 feet in the air. Travel sized eye cream is the solution. This Neutrogena selection is a fan favorite.

Makeup and facial skin can also become oily and dirty while travelling. A quick and refreshing wipe might be just what you need after travelling all day. These Simple wipes are also perfect for removing make-up on the go.

Some planes offer in-flight entertainment if you use your own device. The problem is, holding your phone for 2 hours can be uncomfortable. Light and portable stands like this one will allow you to relax while you enjoy a movie.

Staying hydrated while flying is a MUST. S’wellwater bottles can help you do it in style. One happy customer wrote “Love it! Keeps my drinks ice cold, even in the hot blazing sun.”

Frequent fliers know better than anyone that consolidating items to fit into a carry on makes life so much easier. Space is precious for women that love accessories- so a nice sized tote is a must. This one fits neatly onto roller luggage- and even has a strap to keep it there!

Over 1,300 Amazon customers agree that this bag bungee makes travel so much easier. Effortlessly carry any bag on top of your roller bag using this simple tool.

Frequent fliers know how important organization is. No one wants to deal with toothpastes, hairsprays, and face make up spilling and ruining luggage. With 350 reviews and 4.5 stars, this bag allows space for all your make-up, travel sized hair products, and basic toiletries. Plus, it’s super cute.

No one wants to be stuck on a 4 hour flight while freezing the entire time. Comfy sweaters are the perfect thing to slip on once you board. This one also happens to be stylish.

Basic neck pillows are a thing of the past. Bucky pillows are great for sleeping on the plane and offering lumbar support in the car. They have removable covers and easily attach to your luggae without taking up much space. One customer raved, “These minis are especially great for travel. I have one permanently in my carry-on bag so I’ll never be without it.”

Women have been driving change in the workplace and the home. But there are still key opportunities for continued growth, especially on the money front.

According to a recent report by Merrill Lynch, 41% of women say their biggest financial regret is not investing more. According to the report, the key barriers for women are: 60% cite a lack of knowledge and 34% cite confidence. “Women regret not investing more of their money and are looking for financial education and solutions that align with their values and priorities, as well as their bottom line,” the report states.

Money and Life:

If you’re like most women I know, you take real pride in making your own money. And you should… because you’ve literally earned it. But earning and saving aren’t the only things you should be doing. Investingcan make a heck of a lot of sense for you, too. And I’m not just talking about your 401(k) (kudos to you if you’re contributing) or your IRA (another thumbs up) or even your Roth. I mean investing in you — building wealth starting today so Future You can have the retirement of your daydreams.

Sure, investing can be a little scary (most of us hear about the market fluctuations), but it’s important to remember this is a long game, we’re talking 35-40 years! And if you don’t invest, and just keep your cash under the mattress (or, you know, in a savings account), in the long run, you’ll be losing money. In fact,you could be missing out on $100 a day by waiting to invest. Every. Single. Day.

That’s a fact.

In order to build real wealth, you will need to invest your money over time. The good news: investing is not that scary. You don’t need to be rich to start. And, you certainly do not need to know a whole lot about the stock market to make good investments, especially when there are robo-advisors with algorithms tailored specifically to women’s incomes and life cycles that can help. So what is investing, how do you do it, and, most importantly, why does it even matter?

Keep reading to get the full scoop on why you need to start investing, including what you can do to get started today.

Look at the Numbers

Did you know that historically your money doubles in the market every eight to 10 years? That may not sound like a good deal but stick with us for a second — let’s look at the numbers. If you wanted to save $1,000,000 by the time you retired (assuming retirement is 35 years away) you’d need to save $2,380 each month. But if you wanted to invest your way to a million dollars, you’d only need to save $491 a month. It’s not magic or bogus, it’s compounding. Einstein called compounding the eighth wonder of the world, and we couldn’t agree more.

When I started working my first part-time job, a good uncle encouraged me to open an investment account with a robo-advisor. I took his advice and set up an automatic contribution of just $30 per month. That’s $1 per day. If you’re reading this you can find a way to come up with $1 per day. No matter how small you start, the most important thing is to get started. You can always increase the amount you save over time. I’m saving way more than $30 per month now. But, the idea is to start.

The sooner you get started the easier it will be to get on track for your financial goals, whatever they may be. Even if you have to start small, get started. You may not be rich yet, but you will never be if you don’t get stat investing.

Put Yourself on Autopilot

As I mentioned earlier, automation is the easiest way to save. When you choose how much to put toward your 401(k) — whether it’s a dollar amount or a percentage of your pay — the money goes into your account before it’s taxed and before you even get a chance to think about spending it. You can replicate that process for an IRA and other investment accounts by setting up automatic monthly payments through your bank. Doing this removes the temptation of spending instead of saving.

The first place you should save for retirement is your employer-sponsored 401(k) plan. This money comes directly out of your paycheck before it hits your bank account, so you may hardly notice. You will seriously end up wanting to kick yourself if you get your full company matches each and every year. An employer match is like a raise without doing any extra work and can range from two percent to sometimes as high as 15% of your annual salary depending on your employer. A huge advantage here is the money comes to you pre-tax and, depending on your age and how you invest, could turn into a substantial amount of money later in life. It’s basically free money to you. You’d have to be crazy not to do everything in your power to get every single cent of it each and every year.

If you’re already investing in your company 401(k), good for you. An important question to ask yourself now is “How am I investing?” If you’re looking for help, our friends over at Ellevest will give you (complimentary) recommendations on how to allocate your “outside” retirement accounts, so you can get a more comprehensive investment approach and the best chance for success.

The next step for saving for retirement is an Individual Retirement Account — aka, an IRA. Anyone with earned income can open an IRA. That’s great news, especially if you’re self-employed, or work at a place without a 401(k) plan. Once you open an IRA, it stays in the same place, even when you switch jobs; it’s not housed with your employer.

Here are your IRA options: There’s the traditional IRA, Roth IRA (which comes with income limits), and — if you’re a literal boss and are self-employed — you may want to open a Simplified Employee Pension IRA (SEP-IRA).

Roth vs. Traditional IRA: What You Need to Know

You’ve now made it through the whole 401(k) vs. IRA decision Nice work — that dream retirement is looking a lot more real. Next up: deciding whether you want to use a traditional IRA or a Roth IRA (or both). Here’s what you need to know.

First things first: Not everyone’s eligible to Roth it up. Before we go any further, there’s one big thing you need to know: Not everybody’s eligible to contribute to a Roth IRA. There are income limits. So if your modified adjusted gross income (MAGI) is over $135,000 as a single filer (or $199,000 as a married couple filing jointly), then the whole “Roth vs. traditional” question won’t even apply to you. (In which case, maybe it’s time to upgrade your old IRA … you know, just saying.) Learn more and talk to a financial advisor today. No strings attached.

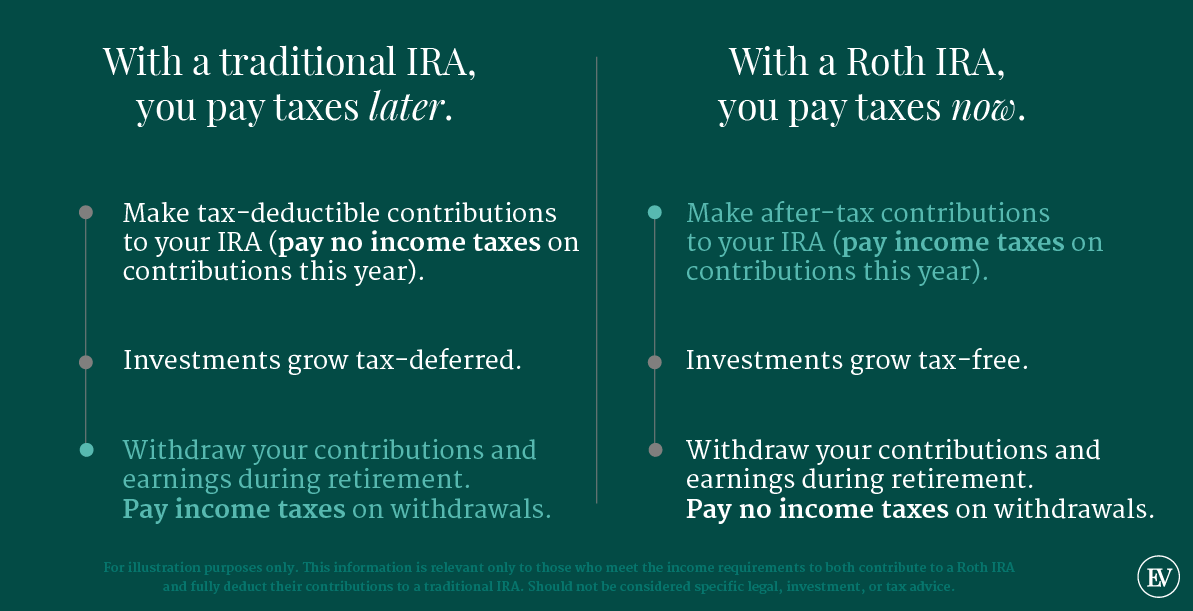

The basic rule with IRAs is you’re going to pay the US government taxes at some point. The question here is when you pay them. With a traditional retirement account, you pay taxes later. With a Roth retirement account, you pay taxes now. So if you think you’ll be in a lower tax bracket when you retire, you might choose a traditional, and if you think you’ll be in a higher tax bracket, you might choose a Roth.

Or, if you have no idea what’s going to happen in the future (what, did you misplace your crystal ball or something?), you might decide to hedge your bets and do a little bit of both according to Ellevest.

Photo: Ellevest

Still not sure which is right for you? Here’s a breakdown of the main ways a traditional IRA and a Roth IRA are similar and different.

How traditional and Roth IRAs are the same

Both traditional and Roth IRAs are retirement accounts with sweet tax benefits. Both allow your contributions to grow tax-free (aka you don’t pay taxes on capital gains, dividends, or interest). And, as long as you’re under the income limits, both allow you to contribute up to $5,500 a year ($6,500 if you’re over 50) — although that’s the limit total, not each. If you have both types of accounts, you can’t put $5,500 into one and $5,500 into the other.

How traditional and Roth IRAs are different

Income limits

There’s no income limit for a traditional IRA; anybody who has an income can open and contribute to one. And if you make under a certain amount, you might be able to deduct them on your taxes (more on that below).

For a Roth IRA, as mentioned above, you’re looking at limits. Single filers with a MAGI over $135,000 aren’t eligible to contribute to a Roth. If your MAGI is between $120,000 and $134,999, you can contribute some, but not the full $5,500. But if your MAGI is under $120,000, you can contribute the full amount to a Roth IRA with no problem. (Married couples and heads of households have different thresholds.)

Age limits

Once you hit age 70½, you can’t put any more money into a traditional IRA. There’s no age limit for Roth IRAs, as long as you or your spouse are still working.

So … traditional? Roth? Both?

If you’re looking for straightforward guidance on which type of account to use, we have good news: When you create a retirement plan with Ellevest, they’ll use the info you give them about your income to see if you’re eligible for a Roth. Then, if you are, they estimate your retirement forecast with a Roth IRA versus a traditional IRA, and then recommend the account type with the higher forecast. (They use the tax brackets that exist today, but there’s always a chance the laws could change.)

Both traditional IRAs and Roth IRAs have their perks, and so it all comes down to your expectations for the future. Basically, if you end up in a higher tax bracket in retirement, you’d be better off with a Roth. And if you end up in a lower tax bracket, you’d be better off in a traditional.

And so, in the end, whichever one you choose is sort of a gamble. Even if you’re right about what will happen with your income, who’s to say that tax brackets will even be the same when you retire? The changes to the 2018 tax code already showed that reform is possible.

One way to try to hedge those bets is to use both account types at the same time. How you split your contributions between the two is up to you. You just can’t pass $5,500 ($6,500 if you’re over 50) in total. And it’s a good idea to talk to a tax pro to really understand what’s right for you.

Whichever account type (or types) you decide to go with, one thing is for sure: When it comes to investing for retirement, the most important thing is that you do it — often and regularly.

Here’s an example of compound interest at work: saving just $100 per month, from 22 to 67, equates to approximately $1,048,000 provided you earn 10% growth per year. Waiting until you’re 32 years old to get started will cause that number to drop to $379,000. As you can see, waiting 10 years will result in a loss of about 64% of your retirement nest egg, all else being equal. (Ok, maybe you shouldn’t expect to earn 10% a year. The point still holds. At a 7% annual return, you’ll have about $379,000 if you get started at 22, but just around $180,00 if you wait until 32.)

The platform is well-designed, easy-to-use, and speaks to our unique financial needs — whether that be planning for retirement, that Aussie vacation, or starting a family. The best part? The advisors at Ellevest are incredibly knowledgeable and will help you every step of the way. Another big bonus? Ellevest has no minimum so you can start with as little as $5 today.

More important than money to is the autonomy to live your life on your own terms — and money can help. Get started today.

This is a lot of information to take in, but take it one step at a time. Trust your gut; do your research. And choose what’s right for you. You’ve got this.

Whether you’ve been diligently studying the runways or simply spent time on the internet recently, you know that fanny packs are back. And while I’m often the first to balk at seemingly over trendy “It items”, when it comes to 90’s accessories, I can see why the fashion world at large has welcomed said fashion accessory.

After all, it’s convenient, super stylish, and versatile. So, where should you get yours? I got my favorites on Amazon. Before you turn away, hear me out.

Amazon is usually not the first place I go when I’m shopping for trend pieces. If you looked at my recent Amazon purchases, it’s a plethora of life items, like toothpaste and Drano.

Lately, though, I’ve been navigating around in the fashion section, and I have to say that I’ve been prettyimpressed by the solid fashion items on offer.

Today we’re adding to the list and sharing the affordable fanny packs we’re adding to our shopping cart before the new season begins.

From iconic brands like Everest and adidas to more undiscovered brands, there’s a selection and style for everyone all under $100. To give you more of a sense of how to wear it, we’re also sharing how we style fanny pack with our favorite outfits. There is, of course, the traditional way to wear it — around your waist. But, lately, we’ve been seeing a few other styling iterations.

For instance, in case you aren’t caught up on your Kendall Jenner style news, she’s suddenly really into fanny packs and wearing it in a new way: across her upper body, like a sling.

Check out the look below, plus, keep scrolling to shop the fashion girl–approved fanny packs we’re adding to our carts.